This post is an excerpt from our 2024 Geography of Cryptocurrency Report. Reserve your copy now!

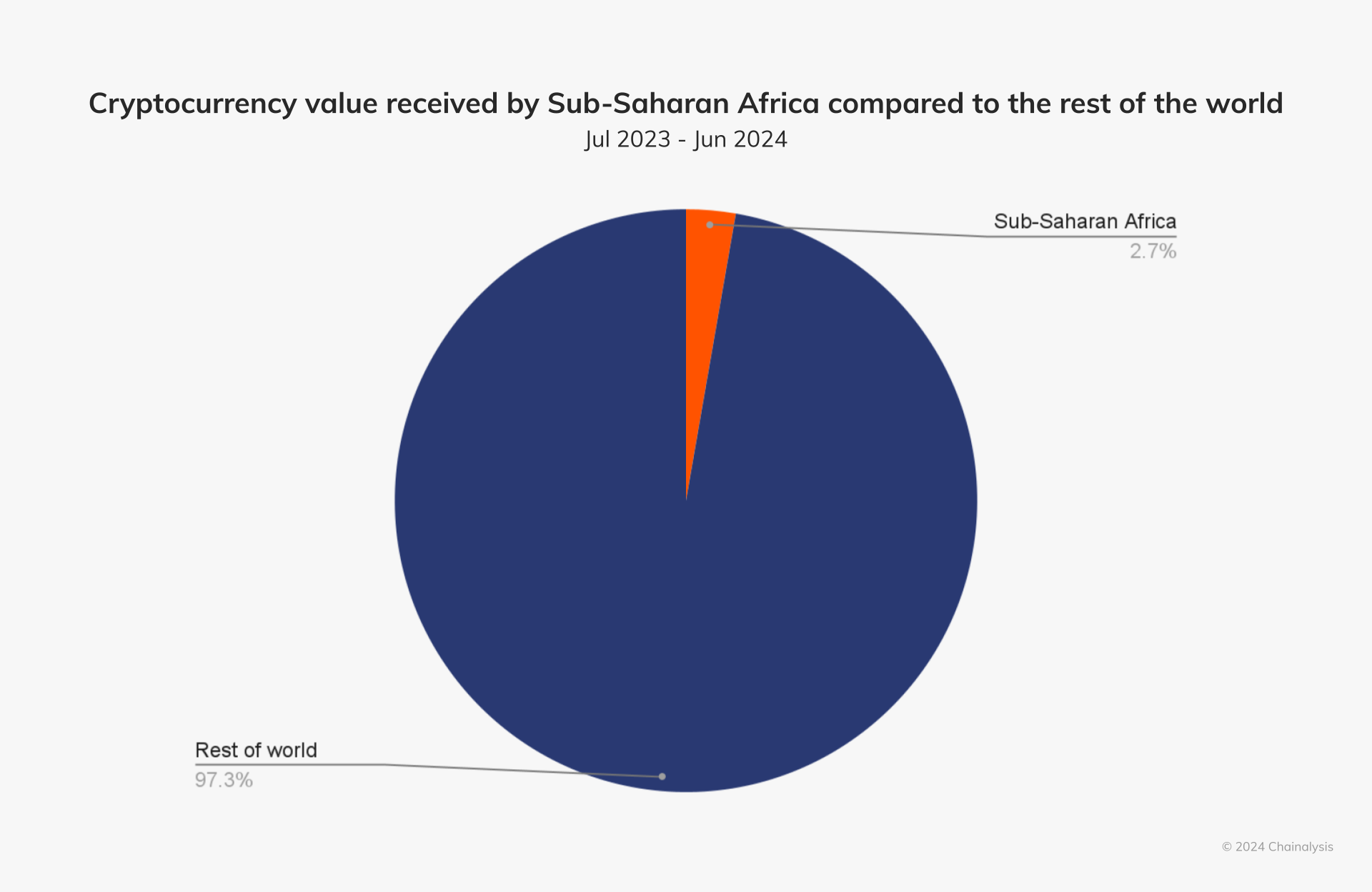

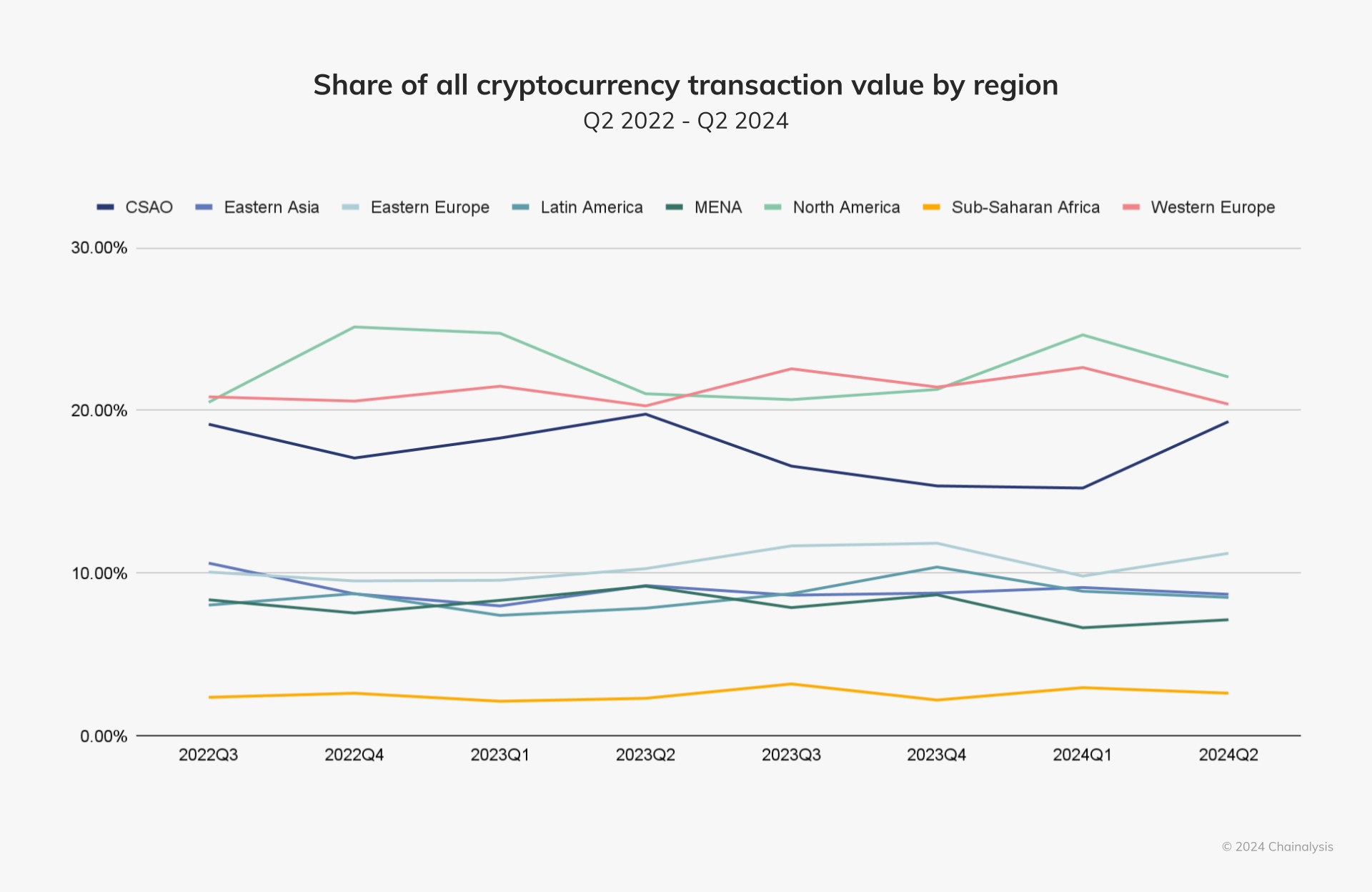

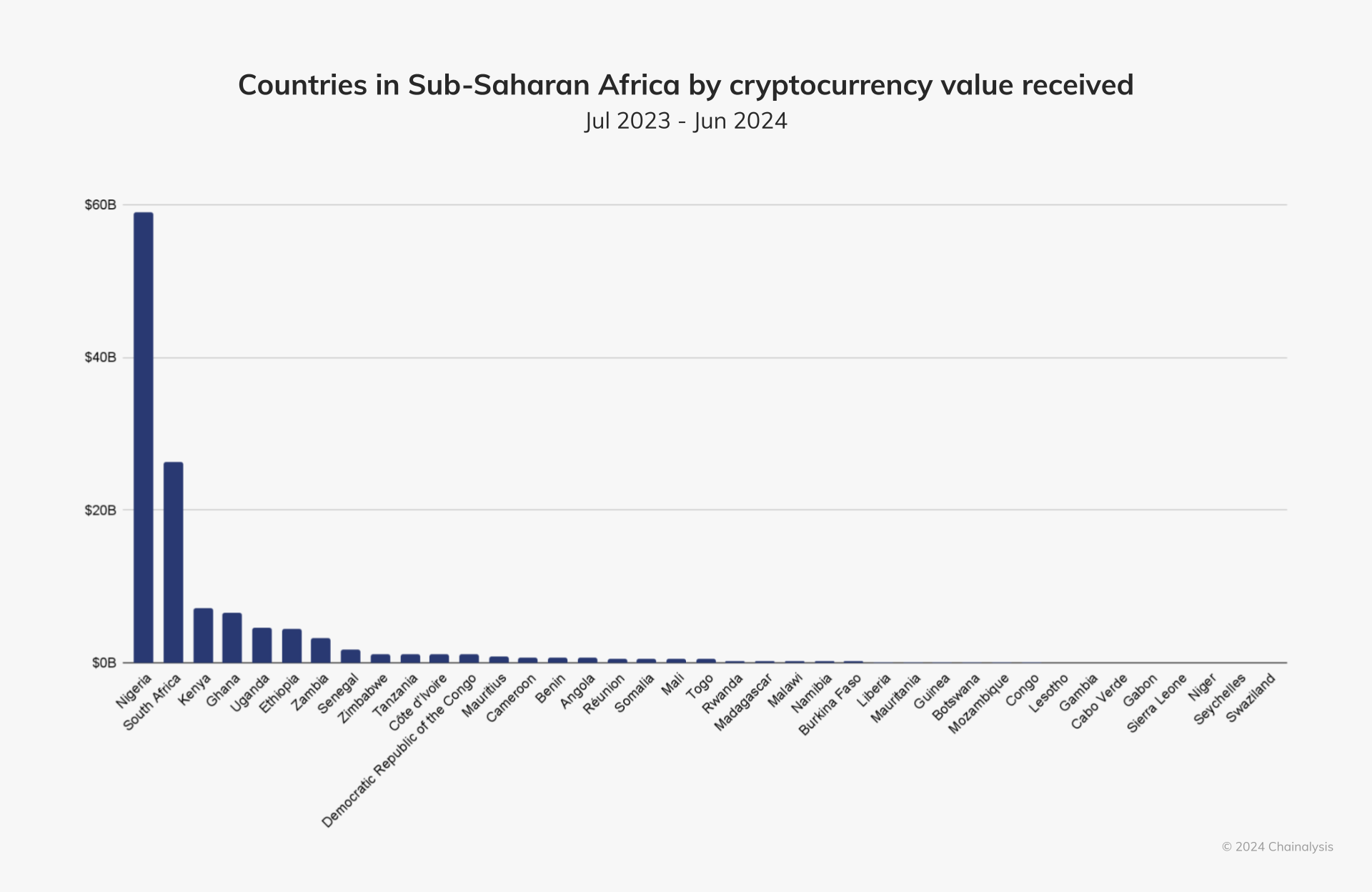

Sub-Saharan Africa accounts for the global cryptocurrency economy’s smallest share, representing 2.7% of transaction volume worldwide between July 2023 and June 2024 — a reflection of the region’s smaller aggregate gross domestic product relative to other regions. Nonetheless, Sub-Saharan Africa saw modest growth, receiving an estimated $125 billion in on-chain value during this period, a $7.5 billion increase compared to last year.

Cryptocurrency is undeniably transforming the financial landscape of the region, home to a number of high ranking nations on our Global Adoption Index. Nigeria maintained its position as a top global player, ranking second worldwide, while Ethiopia (26), Kenya (28), and South Africa (30) also made the top 30.

Crypto’s practical use cases in Africa are especially compelling. Africans are leveraging crypto for business payments, as a hedge against inflation, and for more frequent, smaller (i.e. retail-sized) transfers.

Notably, Sub-Saharan Africa leads the world in DeFi adoption, likely driven in part by a growing need for accessible financial services in a region where only 49% of adults had a bank account as of 2021, according to the World Bank.

Drawing on its position as a frontier for financial innovation and inclusion, Sub-Saharan Africa is emerging as a global model for how crypto can drive real-world impact, especially in areas underserved by traditional financial systems.

Stablecoins are driving economic resilience and global connectivity across Sub-Saharan Africa

Stablecoins have become a key element of Sub-Saharan Africa’s crypto economy. In countries where local currencies are highly volatile and access to U.S. dollars is limited, dollar-pegged stablecoins like USDT and USDC have gained traction, offering businesses and individuals alike a reliable way to store value, facilitate international payments, and support cross-border trade.

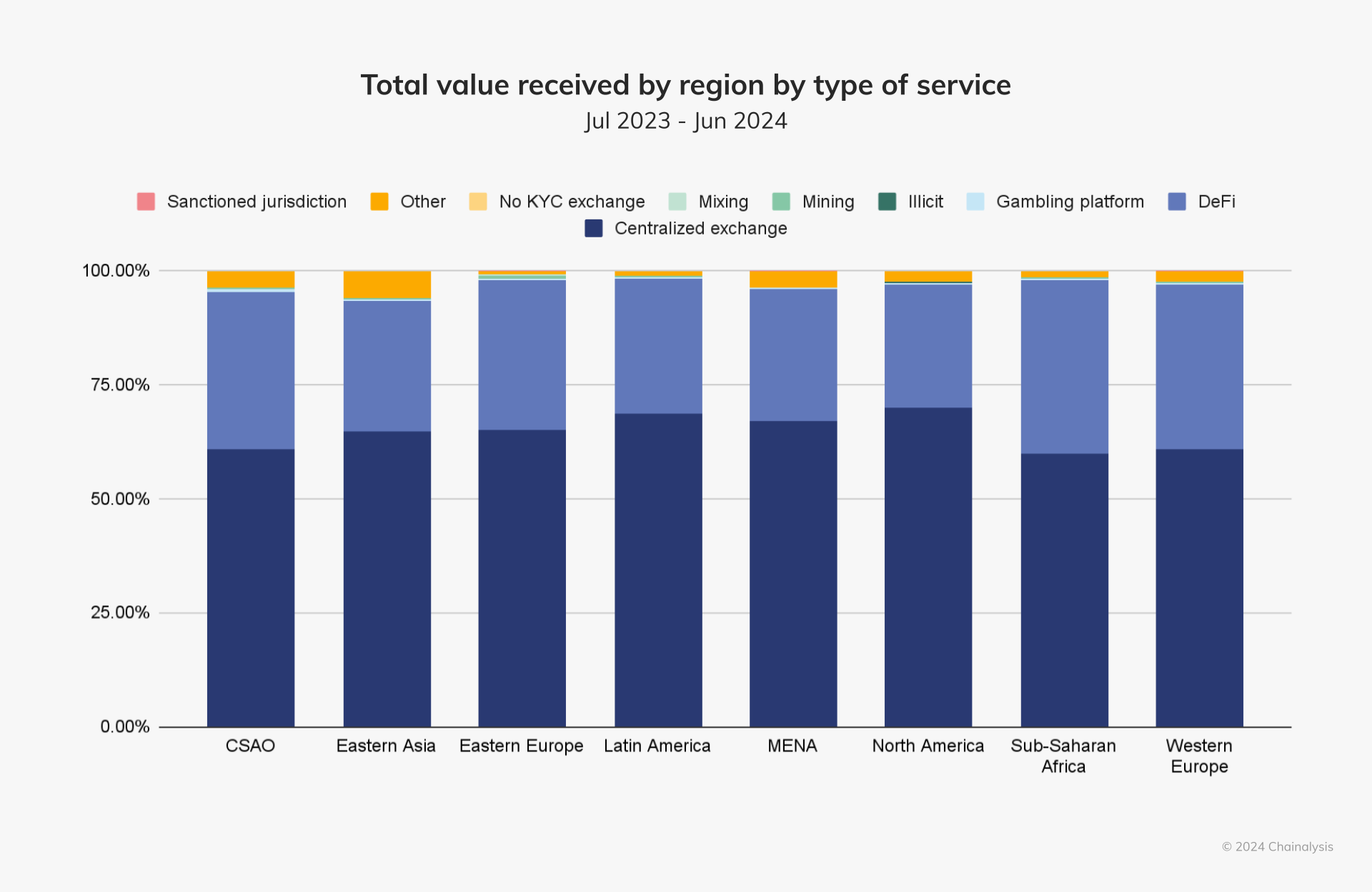

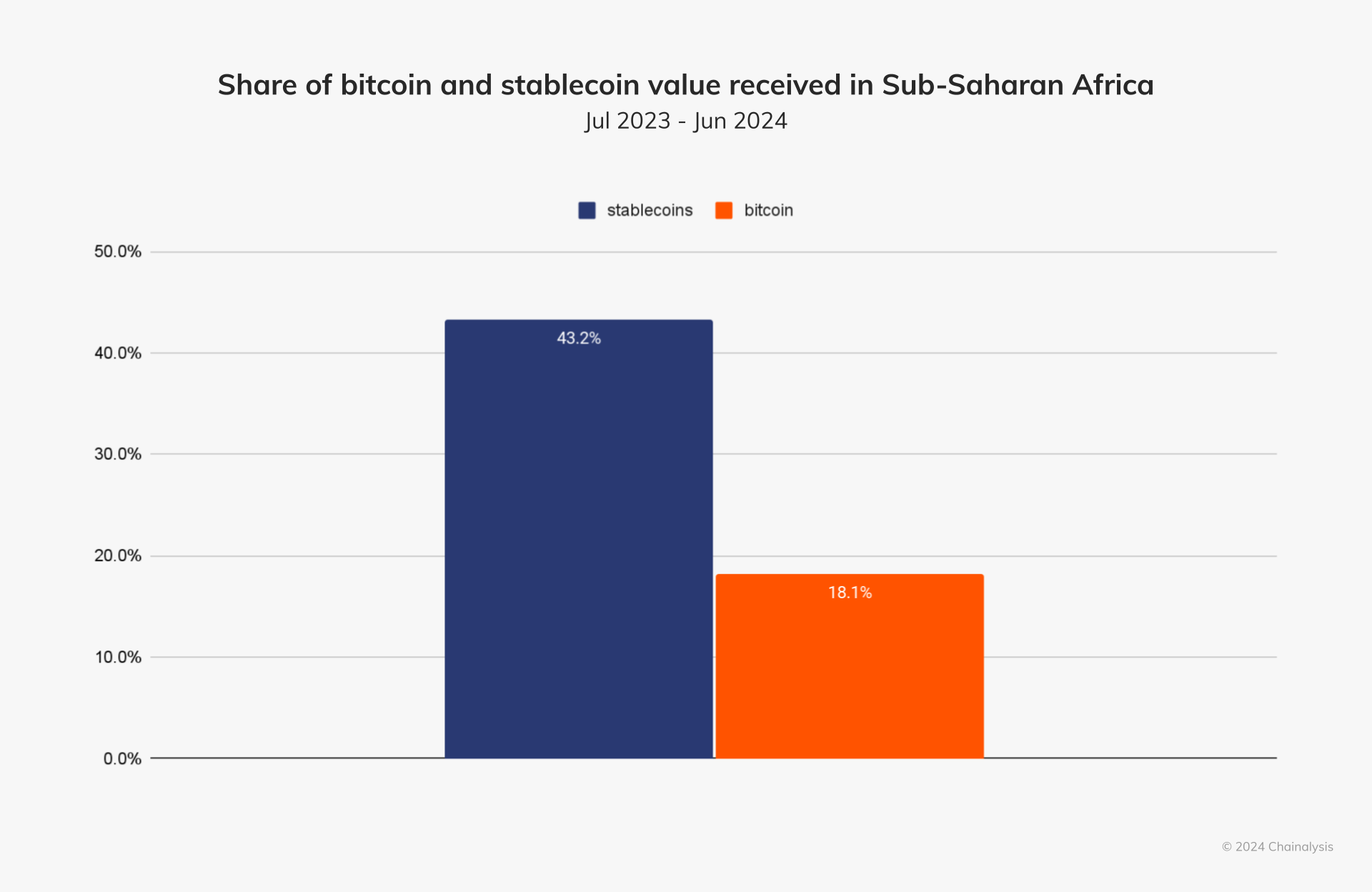

Stablecoins now account for approximately 43% of the region’s total transaction volume.

For further context on the growing prominence of stablecoins, we spoke to two key figures shaping Africa’s crypto landscape: Rob Downes, Head of Digital Assets, ABSA Bank, CIB — a major African bank operating in 12 African countries, and Chris Maurice, CEO and Co-Founder of Yellow Card — one of Africa’s leading crypto-asset exchanges, which operates across 20 countries on the continent.

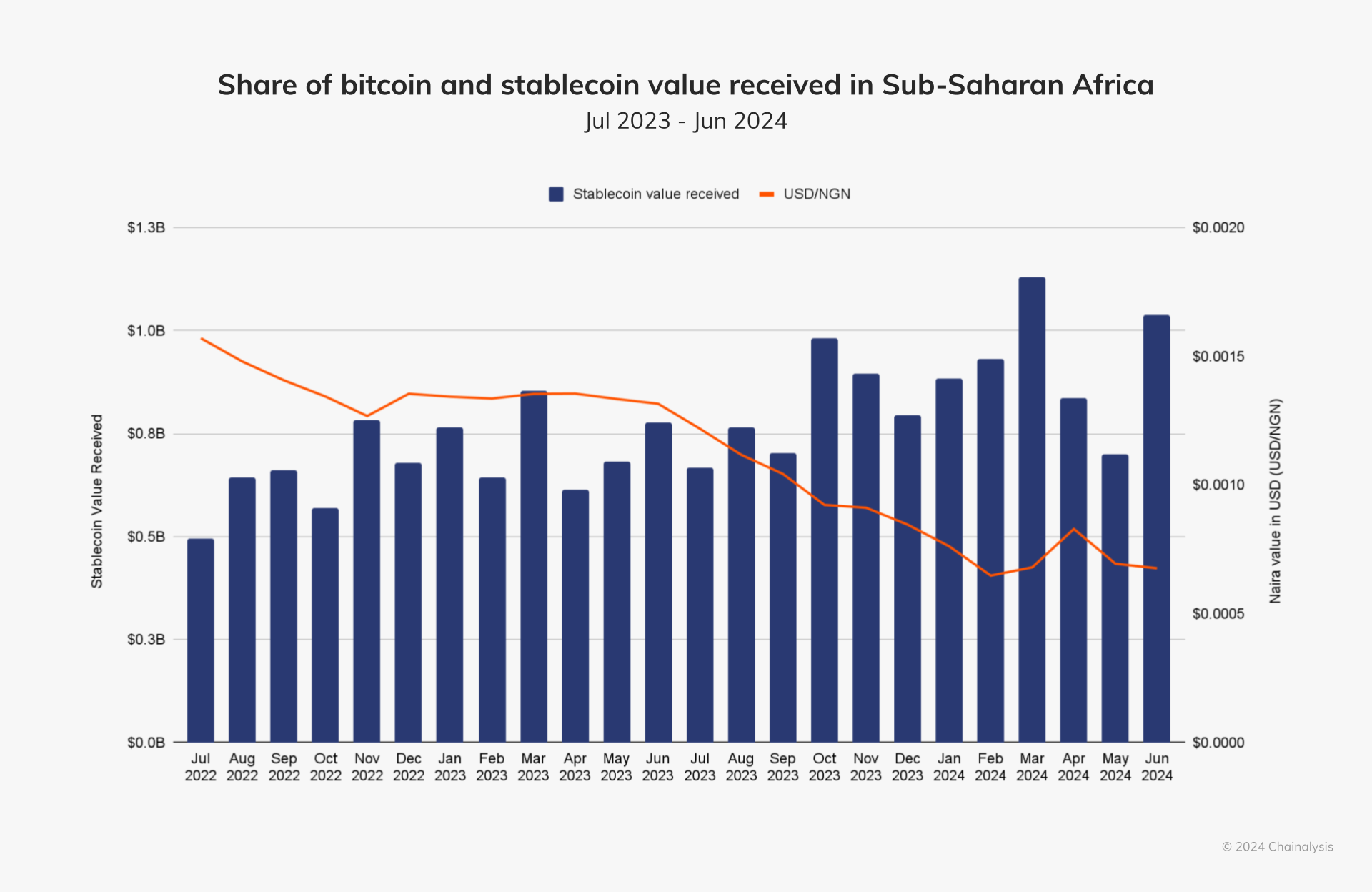

A major driver of stablecoin adoption in Africa is the foreign exchange (FX) crisis gripping many countries. “About 70% of African countries are facing an FX shortage, and businesses are struggling to get access to the dollars they need to operate,” Maurice explained. “Stablecoins provide an opportunity for these businesses to continue to operate, grow, and strengthen the local economy.” Small to medium-sized stablecoin inflows, which we measure under $1 million, tend to align with the naira’s depreciating value, as we see below.

As the naira depreciates, we can see a rise in stablecoin inflows for transactions under $1 million, with more pronounced activity during periods of significant currency devaluation.

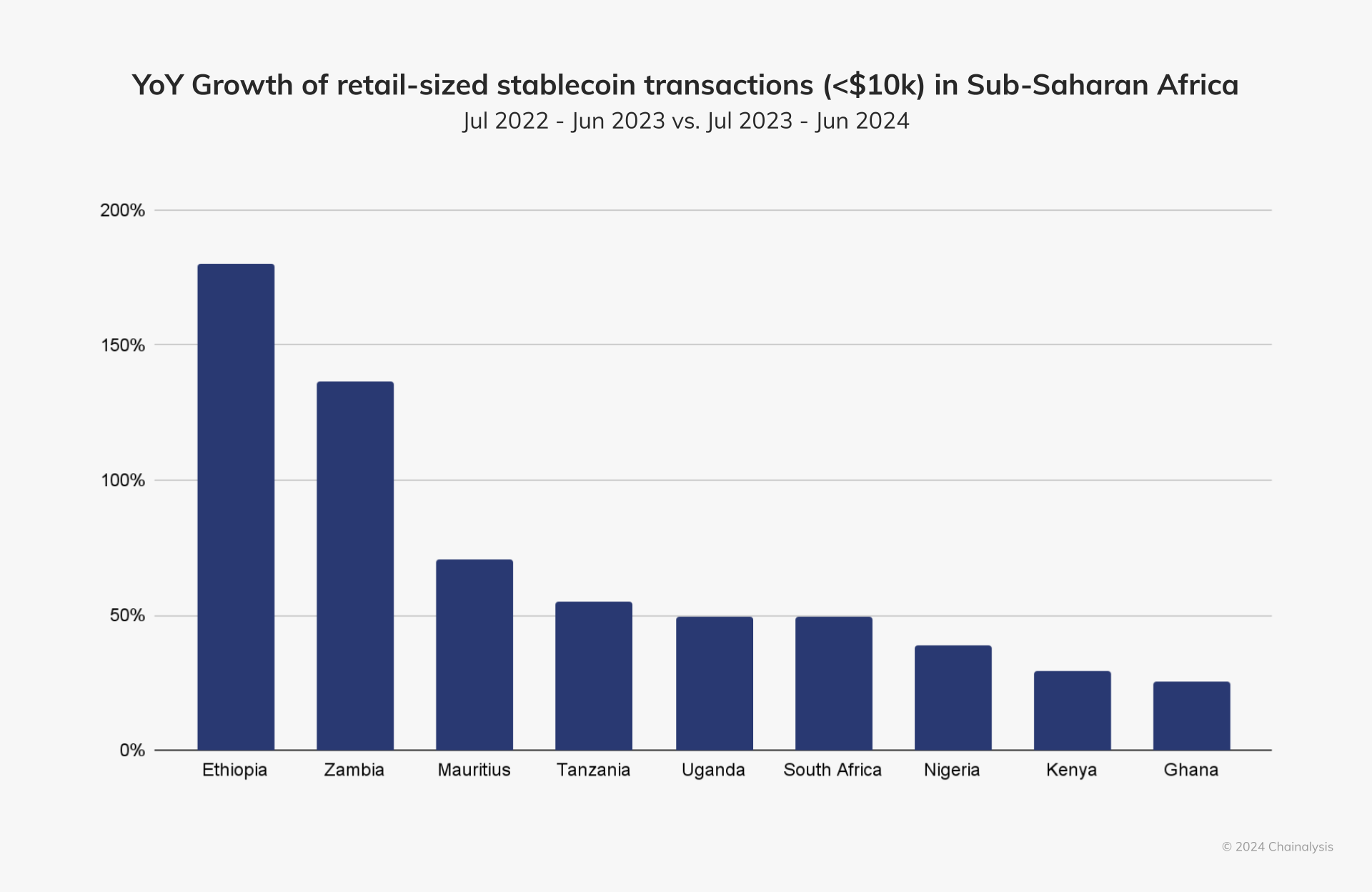

Ethiopia, Africa’s second-most populous nation with 123 million people, is now its fastest-growing market for retail-sized stablecoin transfers, with 180% in growth, year-over-year (YoY).

The birr (ETB), Ethiopia’s local currency, shed 30% of its value in July after the government eased currency restrictions in a bid to secure a $10.7 billion loan from the IMF and World Bank. This loss in value will likely fuel further demand for stablecoins.

For many African businesses, accessing stablecoins through platforms like Yellow Card offers an alternative to traditional financial institutions (FIs) that are unable to meet their demand for U.S. dollars. “Stablecoins are a proxy for the dollar,” Maurice said. “If you can get into USDT or USDC, you can easily swap that into hard dollars elsewhere.” This reality has made stablecoins indispensable for companies involved in international trade. From small-scale importers buying goods overseas, to large multinational corporations importing raw materials from Europe — stablecoins are facilitating transactions that would otherwise be stalled due to currency shortages.

Stablecoins are also revolutionizing cross-border payments across Africa. “People don’t care about crypto,” said Maurice, emphasizing that the focus in the region lies instead on crypto’s practical use cases. He related examples of businesses that Yellow Card serves, such as a major food producer that uses stablecoins to pay suppliers abroad. Additionally, many African fintech companies rely on stablecoins to manage large sums of local currency, which they can then convert into stablecoins to facilitate cross-border payments.

Rob Downes of Absa Group noted a similar trend among institutional clients in South Africa. “Our institutional clients are particularly interested in using stablecoins as a tool for managing liquidity and reducing exposure to currency volatility,” Downes told us. In countries where the value of the local currency fluctuates, stablecoins could be an attractive option for businesses looking to hedge against currency risks.

Downes also pointed to the growing use of stablecoins for remittances and international payments. “We see stablecoins as a game-changer,” he said. For individuals sending money to family members abroad or paying for expenses, stablecoins provide a faster, more affordable alternative to traditional remittance services.

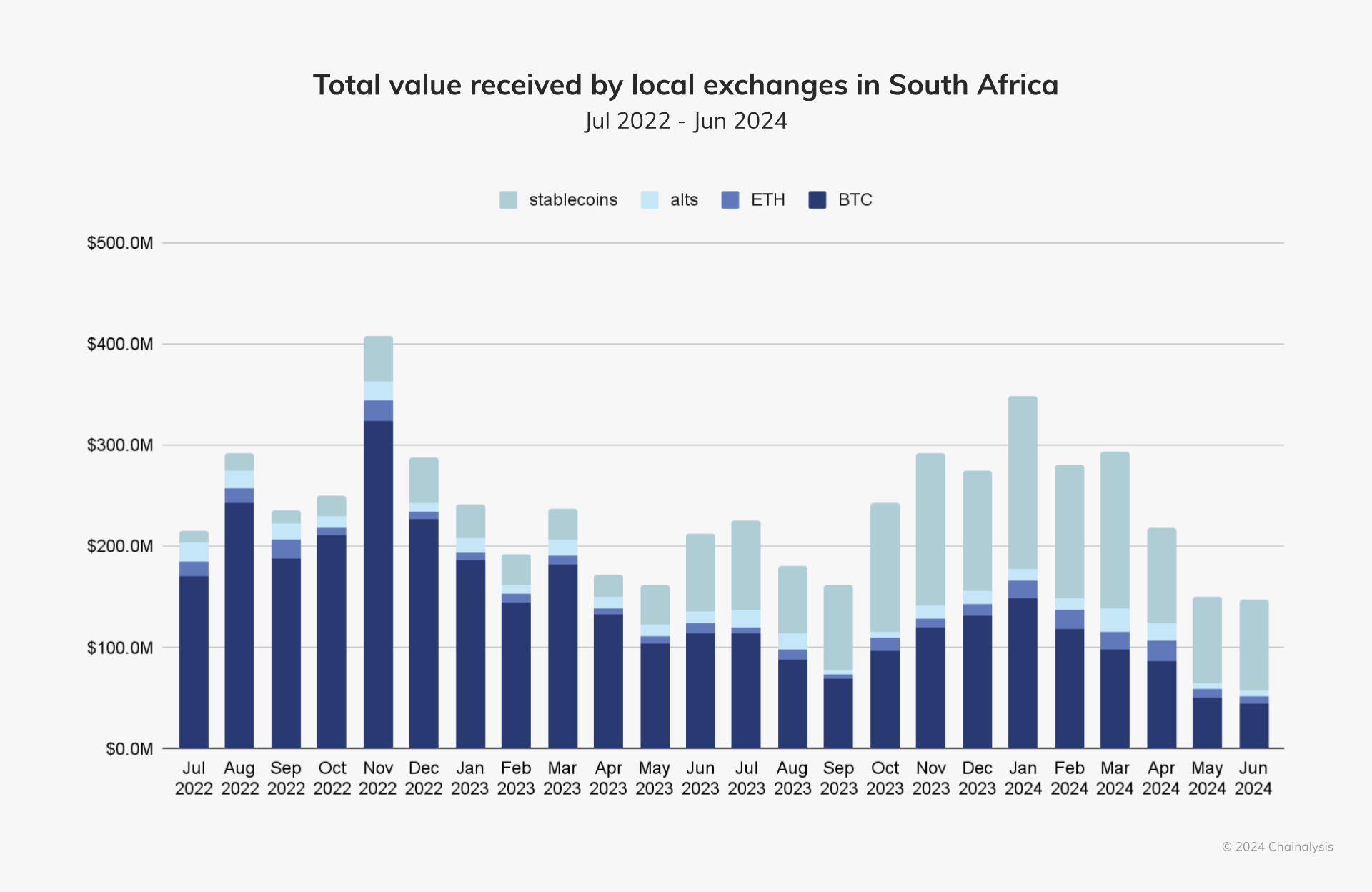

Beginning in late 2023, stablecoins have experienced sustained growth in South Africa’s local exchanges — over 50% month over month in October 2023. Stablecoins have displaced bitcoin as the most popular cryptocurrency received in recent months.

While stablecoin use is expanding rapidly across Africa, the regulatory landscape is progressively evolving. In South Africa, the Financial Sector Conduct Authority (FSCA) has provided regulatory clarity by classifying crypto assets as financial products, although there are no specific regulations for stablecoins. “We’re working closely with regulators like the [South African] Reserve Bank to ensure we’re prepared for any developments around stablecoin regulation, which we expect will be a major area of focus soon,” Downes added. Maurice pointed out that, in many cases, stablecoins operate in a “gray area,” where they are neither explicitly regulated nor prohibited. He emphasized the importance of working with regulators to ensure stablecoin users remain compliant. “We do quite a bit of work with regulators on the ground,” Maurice said. “We’re working with central banks and financial authorities across 20 countries to help them understand how stablecoins can be used safely and effectively.”

Looking towards the future, both Downes and Maurice see stablecoins continuing to play a central role in Africa’s economy. “I think stablecoins are going to be the primary use case for crypto in South Africa over the next three to five years,” Downes said.

Maurice echoed this sentiment, adding that stablecoins are helping to open up African economies to global markets. “Stablecoins are actually developing a market for African currencies that have never had an international presence,” he said. By providing a way for businesses to transact in non-volatile currencies, stablecoins are fostering greater price transparency and encouraging foreign investment. “It’s creating more of an open economy that actually encourages investment,” Maurice added.

Nigeria is ground zero for crypto activity in Sub-Saharan Africa

In recent years, Nigeria has emerged as a global leader in crypto adoption, driven by innovative use cases to combat economic challenges. Ranking second overall on our Global Adoption Index, the country received approximately $59 billion in cryptocurrency value between July 2023 and June 2024.

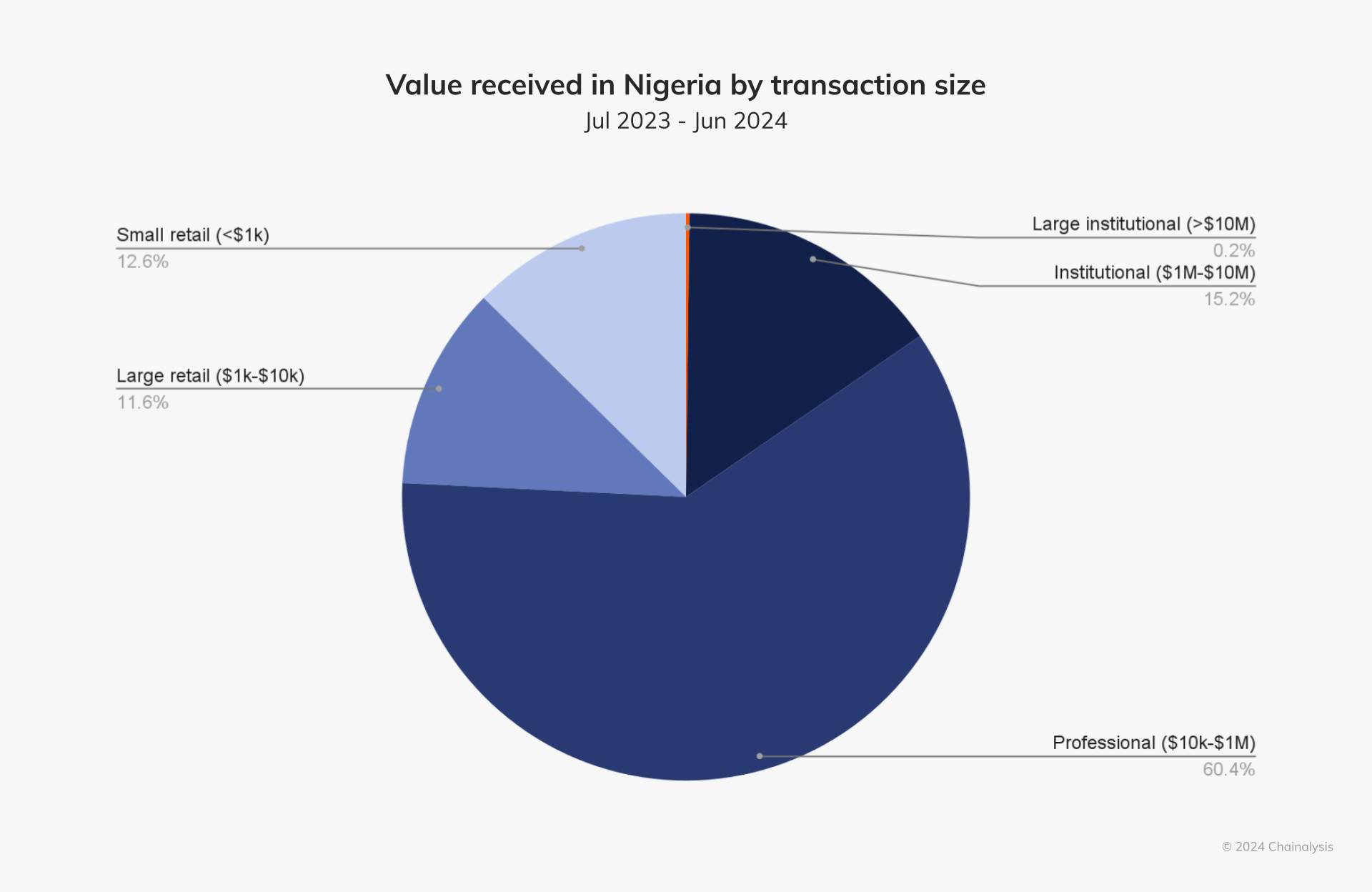

Nigeria’s crypto activity is largely driven by smaller denomination retail and professional sized transactions, with around 85% of the value of transfers received under $1 million.

We spoke with Moyo Sodipo, COO and Co-founder of Busha, a crypto exchange with a presence in Nigeria, to get an on-the-ground perspective of the country’s crypto adoption. Everyday activities like bill payments, mobile phone credit top-ups, and retail purchases are increasingly being powered by crypto, according to Sodipo. “People are starting to see the real-world utility of cryptocurrency, especially in day-to-day transactions, which is a shift from the earlier view of crypto as just a get-rich-quick scheme,” he explained.

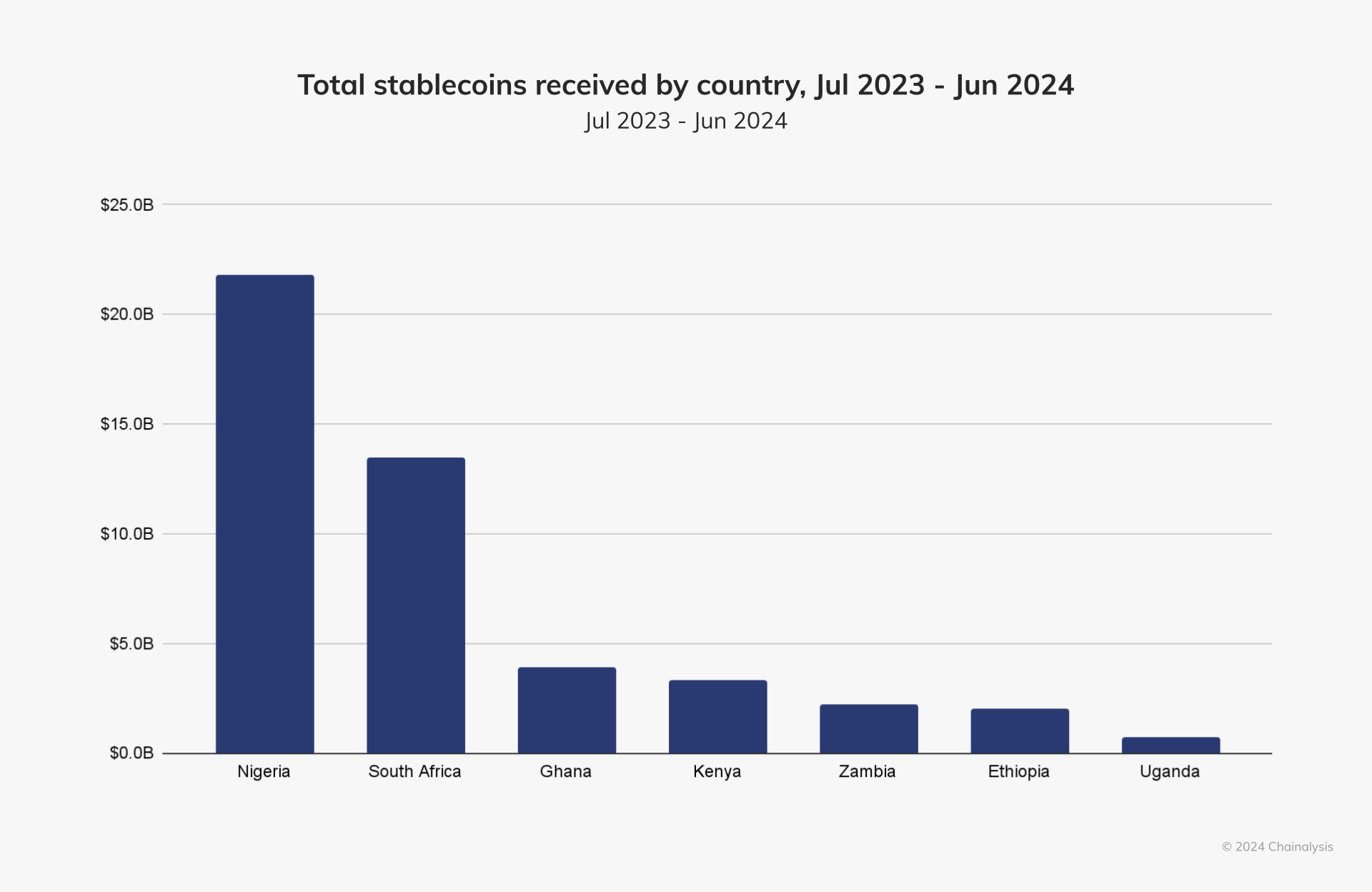

As in Ethiopia, Ghana, and South Africa, stablecoins are also a major part of Nigeria’s crypto economy, accounting for approximately 40% of all stablecoin inflows in the region — by far the highest in all of Sub-Saharan Africa.

Many Nigerians rely on stablecoins to send money across borders due to the inefficiencies and high costs associated with traditional remittance channels. “Cross-border remittances are a major use case for stablecoins in Nigeria,” Sodipo noted. “It’s much faster and more affordable.”

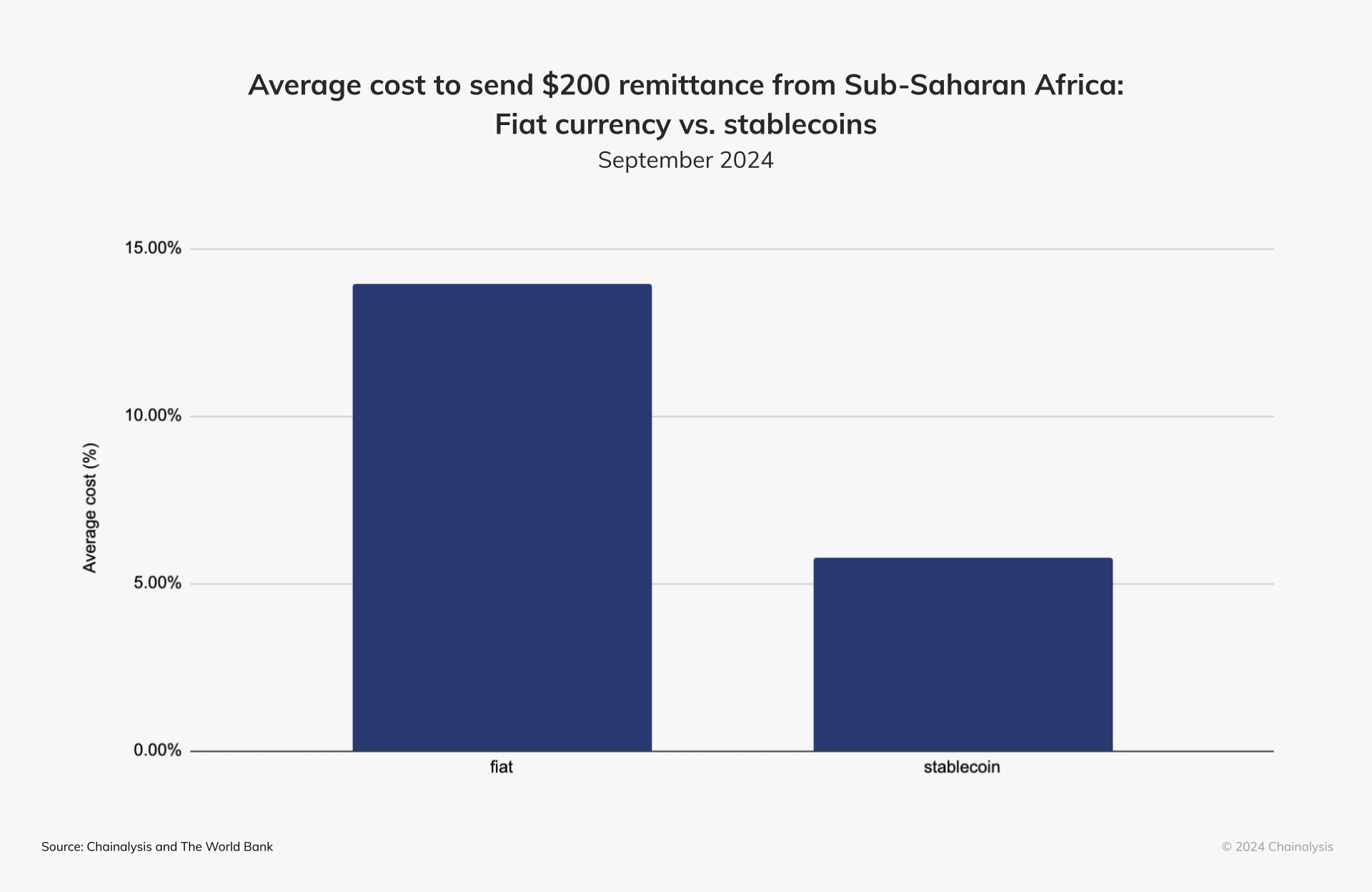

As shown below, the average cost of sending a $200 remittance from Sub-Saharan Africa is approximately 60% lower when using stablecoins compared to traditional remittance methods facilitated by fiat currency.1

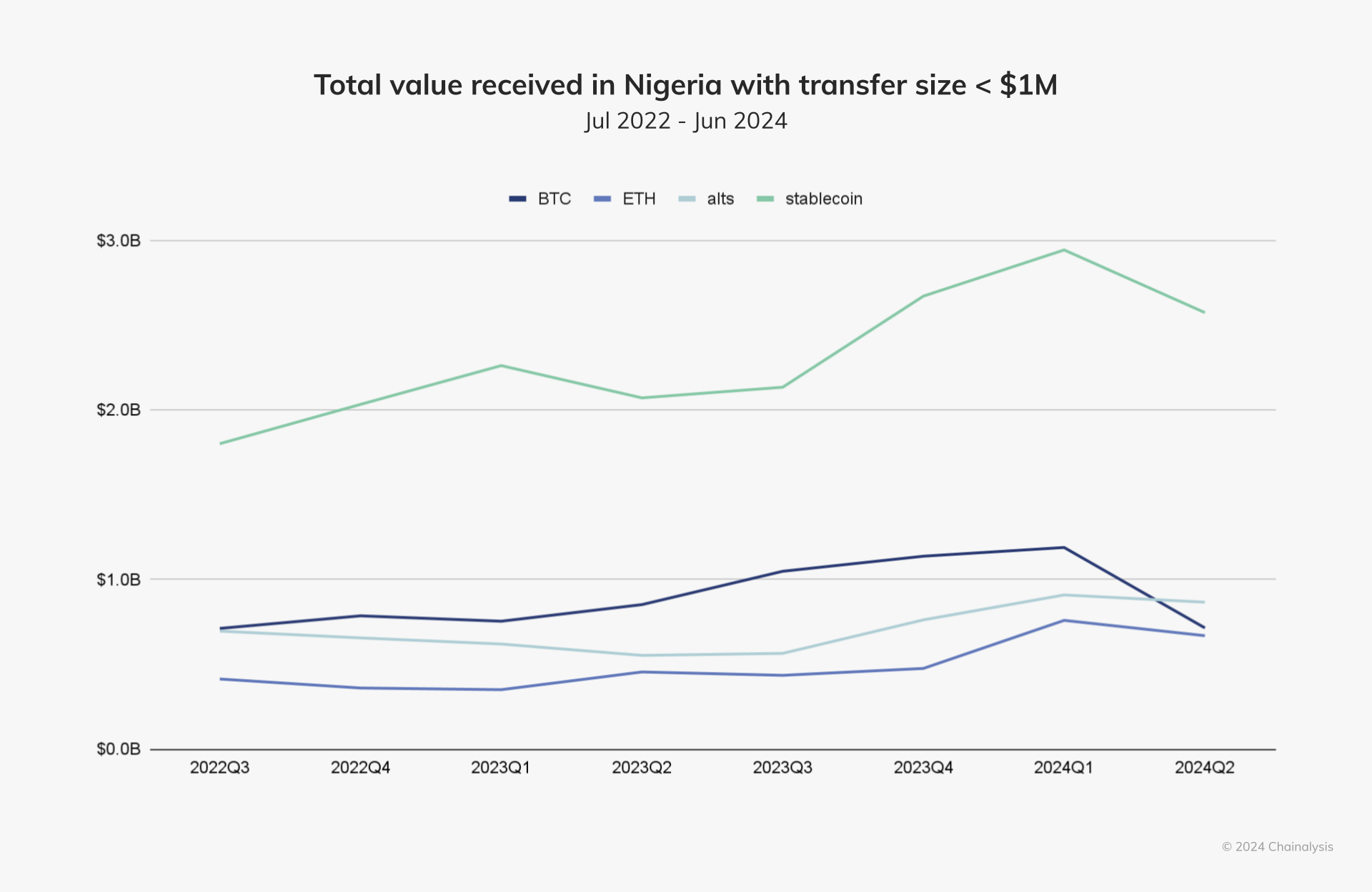

As in other African countries, a major driver of stablecoin adoption in Nigeria is inflation and the depreciation of the naira — which plummeted to a record low in February 2024. We can see the impact of this trend by looking at transfer sizes under $1 million. In Q1 2024, stablecoin value approached almost $3 billion, making stablecoins the largest portion of sub-$1M transactions in Nigeria.

Although bitcoin and altcoins remain relevant, representing billions in value received, stablecoins are clearly becoming the preferred medium for small to medium sized transactions, suggesting adoption on a broad scale.

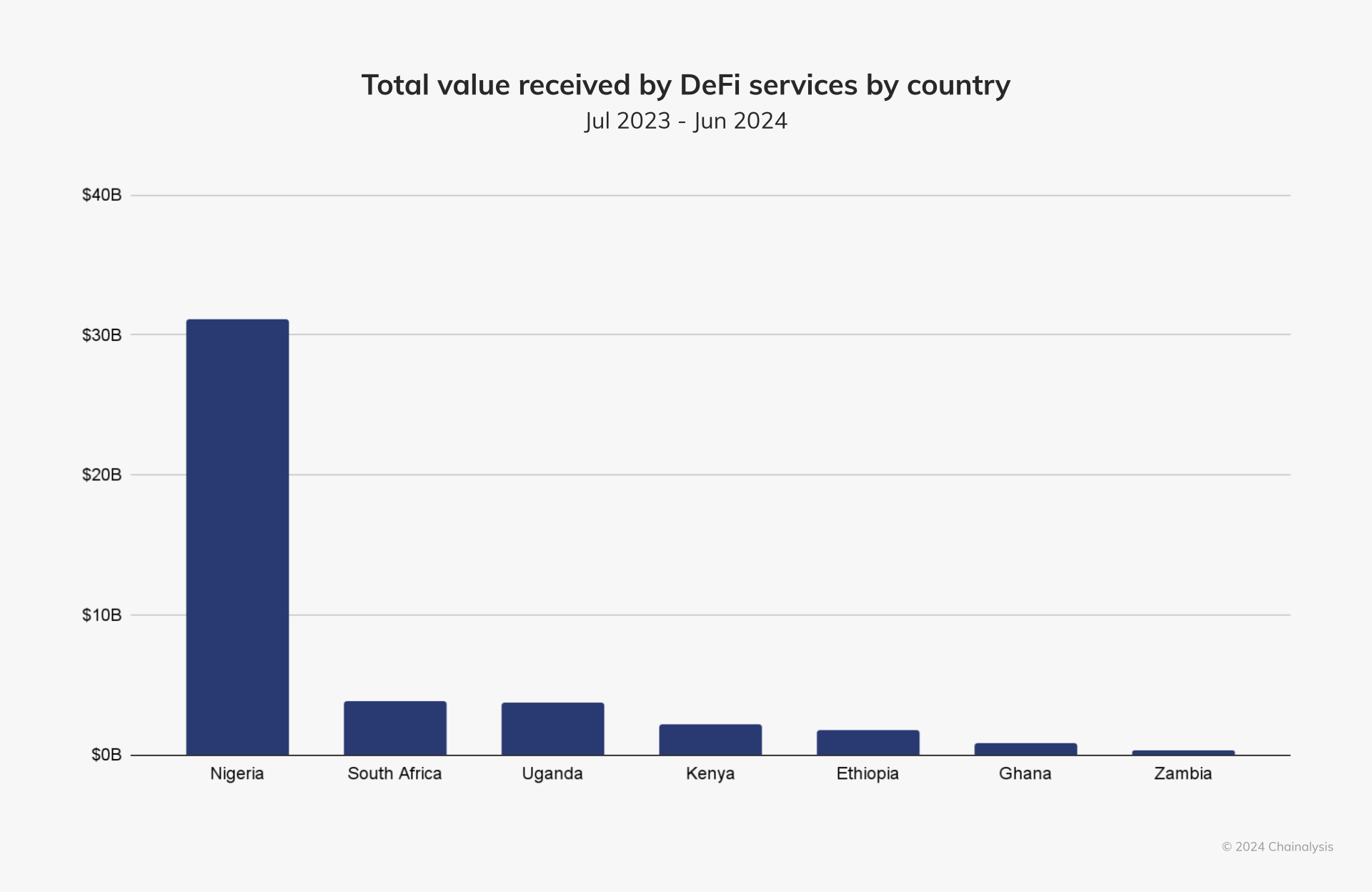

In addition to the rising prominence of stablecoins, DeFi is experiencing a major moment in Nigeria, echoing the broader trend of Sub-Saharan Africa as the global leader in DeFi adoption. Nigeria stands at the forefront of this trend, with over $30 billion in value received by DeFi services last year.

DeFi platforms are providing Nigerians with new opportunities to earn interest, take out loans, and engage in decentralized trading, in addition to the traditional financial systems. “DeFi is a key area of growth, as users explore ways to maximize returns and access financial services that might otherwise be unavailable to them,” said Sodipo.

The December 2023 lift of the central bank’s ban on banks serving crypto companies has also played a pivotal role in this momentum. “Since the banking ban was lifted, it has opened up a lot of possibilities for partnerships and smoother transactions,” Sodipo explained. Building on this development, in June 2024, the Securities and Exchange Commission (SEC) of Nigeria introduced its Accelerated Regulation Incubation Program (ARIP), which now requires all virtual asset service providers (VASPs) to register and undergo an assessment before full approval. “The industry is bullish on ARIP; it’s a shift away from uncertainty and a positive move towards regulatory clarity,” said Sodipo.

While Nigeria is making progress with initiatives like ARIP, many FIs remain hesitant to fully engage with the crypto sector due to lingering regulatory ambiguities. “Banks are still cautious, waiting for clear signals from the central bank and SEC before fully entering the market,” Sodipo explained.

Nonetheless, Nigeria’s crypto market continues to flourish. Looking ahead, Sodipo is optimistic about crypto’s future in Nigeria, particularly amid ongoing regulatory reforms. “The open dialogue with regulators is key. We’re hopeful that further clarity will drive more banks and financial institutions into the space,” Sodipo said.

South Africa’s crypto market thrives, spurred by growing institutional activity and TradFi involvement

As Africa’s largest economy, South Africa has established itself as one of the continent’s largest cryptocurrency markets, receiving approximately $26 billion in value over the past year. South Africa is seeing notable growth in licensed companies and increased institutional-sized activity.

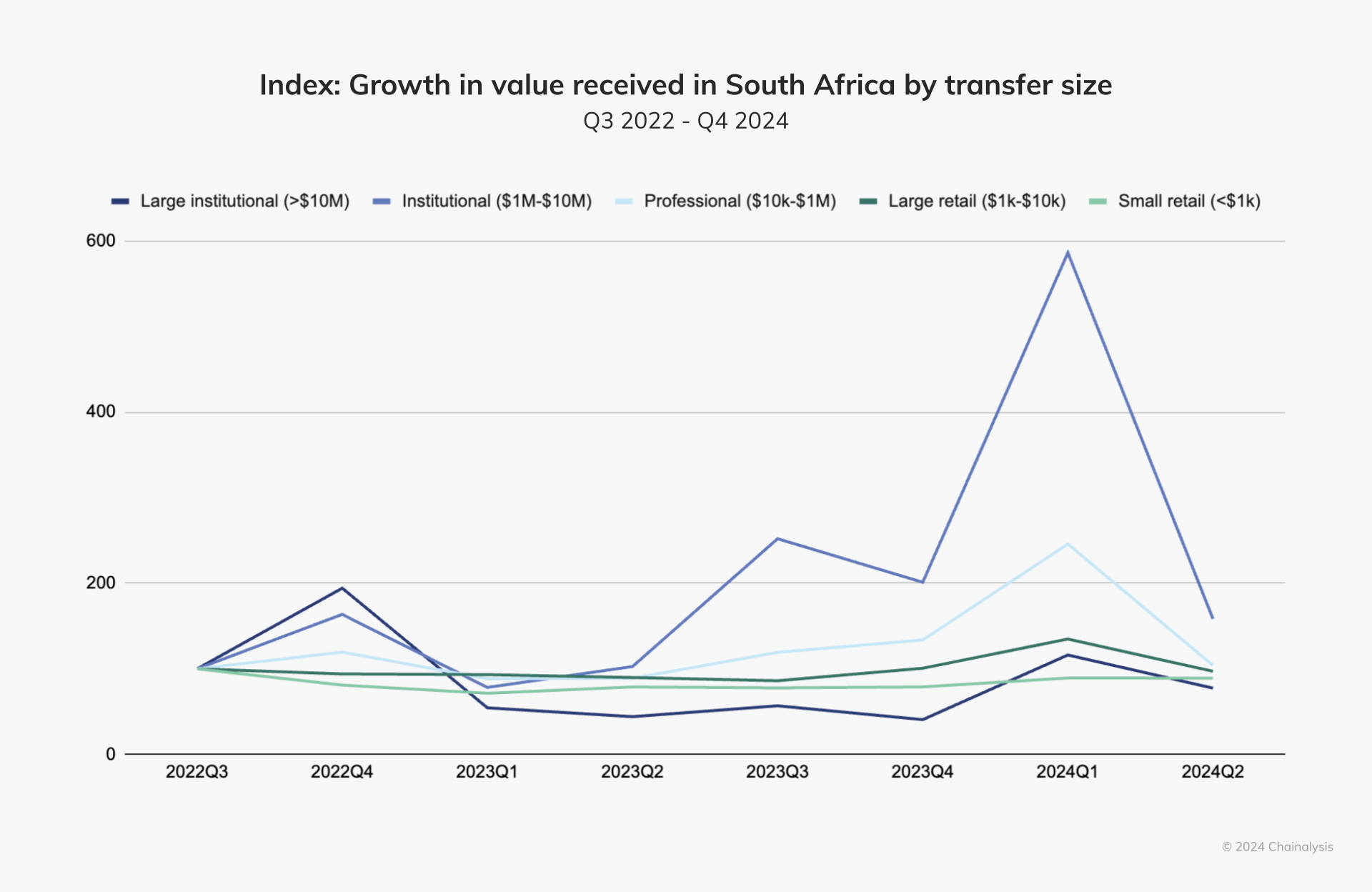

The chart below shows the growing impact in South Africa of institutional and professional-sized transactions, which have become the largest contributors to total indexed value received, especially from late 2023 through Q1 2024.2

This TradFi-crypto nexus has notably been picking up steam in South Africa. According to Rob Downes of Absa Group, South Africa is at a pivotal moment where traditional finance and digital assets are beginning to converge. “We are seeing growing interest from institutional clients, particularly around custody solutions for digital assets, which will play a crucial role in supporting the crypto ecosystem here,” Downes said.

Although institutional players are driving much of the market activity, there is still steady retail and professional engagement. For insight into the business climate, we spoke with Carel van Wyk, founder of MoneyBadger, a company focused on integrating crypto payments for retailers. Van Wyk noted that South Africa’s crypto market has been maturing steadily, particularly in the

payments space. “In the past, people tried to make payments on-chain, but it was impractical because blockchain transactions can become expensive and aren’t suitable for small, fast transactions.” He spoke to advancements in layer2 technologies and payment APIs that have made crypto payments more viable for everyday use, allowing retailers to accept crypto while settling in fiat.

The FSCA’s decision to regulate crypto assets under existing financial laws has been a major catalyst for the market’s growth. This has provided much-needed clarity for both businesses and investors, enabling licensed companies to grow responsibly and encouraging FIs to explore crypto services. “The regulatory environment here is relatively favorable compared to other regions. It’s giving us the confidence to explore more robust solutions like custody and payments,” Downes said.

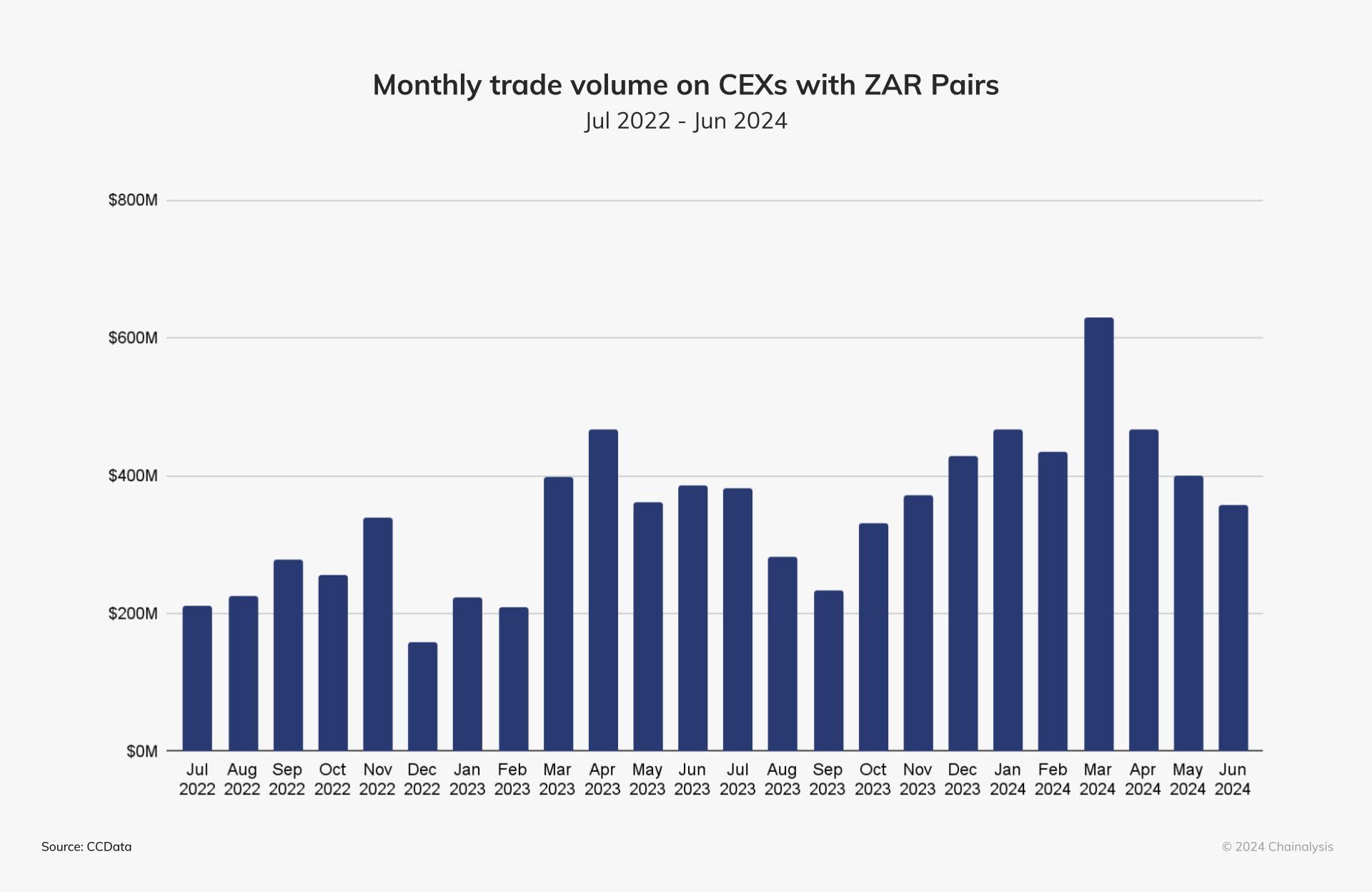

Trading pairs with The South African Rand (ZAR) have also thrived, trading hundreds of millions in value monthly.

The performance of ZAR pairs demonstrates South Africa’s maturing crypto ecosystem, which Downes believes will drive further institutional engagement. “We’re seeing exchanges becoming more sophisticated, and that’s important for building trust with both retail and institutional investors,” he explained.

South Africa’s regulatory clarity and market growth have attracted the interest of financial institutions. Absa Group Bank, one of the country’s largest banks, is actively exploring blockchain and cryptocurrency initiatives. Downes highlighted that Absa Group’s primary focus is on offering institutional-grade crypto custody services, which they see as a key near-term opportunity. “The thing that I am most excited about — and the biggest near-term revenue opportunity for us — is custody,” Downes shared. Absa Group sees secure custody services as the foundation for institutional crypto adoption, providing security and compliance for exchanges, investment firms, and other large market players.

Absa Group and other South African banks have increasingly shown interest in engaging with the crypto sector, although challenges remain around risk management and compliance. Downes acknowledged that banks need to develop trusted relationships with crypto exchanges and service providers to facilitate services like banking and payments. Downes says that Absa Group has adopted a “learn and experiment” approach, which has gained support from leadership. “We deliberately positioned our efforts as relatively light-touch, focusing on learning and engaging with the market,” Downes explained. This exploratory approach has allowed Absa Group to participate in regulatory sandboxes and collaborate closely with regulators to ensure compliance while advancing their blockchain initiatives.

Customer demand for crypto-related services is steadily increasing. “The inquiries have tripled over the last 18 months,” Downes noted, adding that this interest spans crypto payments, investments, and banking services for exchanges. Institutional clients, particularly family offices and asset managers, are beginning to explore how they can integrate digital assets into their portfolios. “Traditional finance institutions are still relatively early in the crypto space, but the demand from clients is pushing us to move faster,” Downes added.

As banks like Absa Group continue to innovate and explore blockchain technology, they are helping bridge the gap between traditional finance and crypto. “Traditional finance institutions are uniquely positioned to help usher in blockchain-based finance by leveraging our regulatory expertise and controls,” Downes said. As the technology becomes more integrated, both corporate and consumer adoption will accelerate, further solidifying South Africa’s role in the global crypto economy.

A pivotal juncture for Sub-Saharan Africa

Although it represents a relatively small portion of the global crypto economy, Sub-Saharan Africa is experiencing remarkable momentum. Nigeria and South Africa are leading the way, driving substantial on-chain activity and positioning the region as an increasingly influential hub for cryptocurrency adoption and financial technology.

Stablecoins have become a key part of Sub-Saharan Africa’s crypto story, a welcomed hedge against long standing inflation and currency devaluation, now accounting for a majority of crypto transactions across the continent. Simultaneously, DeFi is booming, with the region leading in global adoption of decentralized platforms.

While countries like South Africa, Nigeria, Ghana, Mauritius and Seychelles are making significant progress in establishing regulatory frameworks, others are exploring regulatory pathways in light of increasing exchange volumes and crypto demand. As diverse market players, including banks and other FIs deepen their involvement, the need for clear regulations has never been more urgent.

Africa’s real-world crypto use cases carry valuable lessons for the global market. With a vibrant fintech landscape, expanding mobile penetration, and potential for collaboration between regulators, TradFi, and crypto companies, the continent is well-positioned to emerge as a global crypto leader, with immense promise to drive innovation and financial inclusion on a large scale.

1 The remittance price for fiat currency, sourced from the World Bank for 2024 Q1, is used to represent the average cost for senders, which covers banks, money transfer operators (MTOS), mobile operators, and post offices. For stablecoin remittances, the total cost was calculated to include exchange deposit fees, trading fees, transfer fees, and on-chain transactions on regional exchanges in Sub-Saharan Africa. Both methods account for the FX margin, which reflects the percentage difference between the remittance service provider’s exchange rate and the interbank rate. For stablecoins, the FX margin was calculated using the price difference between the close price on September 18th and the mid-market exchange rate on September 19th at 12:00 AM UTC, as provided by Wise.

2 The spike in institutional inflows at the end of 2023 through Q1 was likely driven by the broader market rally surrounding the U.S. approval of bitcoin ETFs along with the news that the first crypto asset service provider (CASP) licenses would be issued in South Africa, driving sentiment that investing was regulated and protected.

This website contains links to third-party sites that are not under the control of Chainalysis, Inc. or its affiliates (collectively “Chainalysis”). Access to such information does not imply association with, endorsement of, approval of, or recommendation by Chainalysis of the site or its operators, and Chainalysis is not responsible for the products, services, or other content hosted therein.

This material is for informational purposes only, and is not intended to provide legal, tax, financial, or investment advice. Recipients should consult their own advisors before making these types of decisions. Chainalysis has no responsibility or liability for any decision made or any other acts or omissions in connection with Recipient’s use of this material.

Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information in this report and will not be responsible for any claim attributable to errors, omissions, or other inaccuracies of any part of such material.