This blog is a preview of our Guide to On-Chain User Segmentation for Crypto Exchanges. Sign up here to download the full report!

With Bitcoin’s price up over 50% in 2023, crypto winter may be thawing, but business is still tough nonetheless for exchanges.

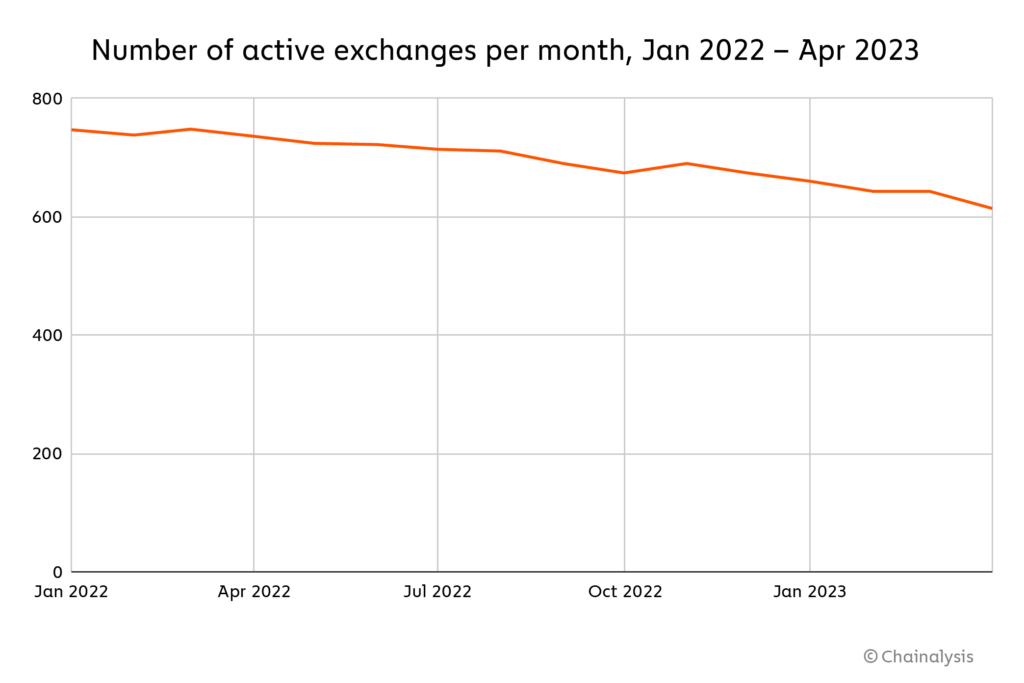

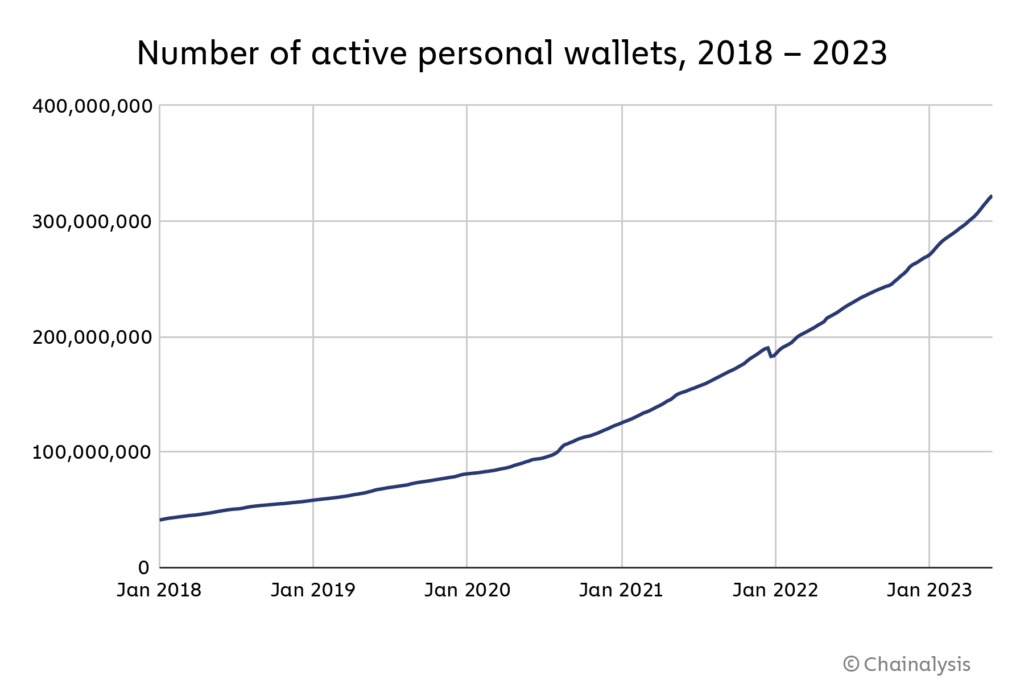

Since the start of 2022, the number of active centralized cryptocurrency exchanges has fallen from 750 to 640, due to pressure from decreasing transaction volumes amidst harsh market conditions, and ever-increasing competition from decentralized exchanges (DEXes). However, at the same time, the number of cryptocurrency users is still increasing. We approximate that growth on the graph below, which shows the number of active or balance-holding personal wallets — also known as unhosted wallets, as they are not hosted by a service and are under the sole control of the owner — across all blockchains Chainalysis supports over the last five years.

Exchanges who can win over the crypto users behind those wallets and take market share now will be in the best position to reap the rewards when crypto winter ends and transaction volumes pick up again. But not all users are the same. Exchanges need to segment their users, and focus on onboarding and retaining the ones that will drive the best outcomes for their business.

Luckily, cryptocurrency’s inherent transparency allows exchanges to segment more effectively than in any other industry. Only in cryptocurrency can you see the holdings, transaction habits, and product preferences of your users and prospects in real time. Armed with that data, exchanges can make data-driven decisions about where to focus their user acquisition and retention efforts. How exactly can they do it? In this guide, we’ll lay out a sample model for exchange user segmentation based on on-chain data, and show you how those segments translate into insights that can drive ROI in exchanges’ user acquisition and retention strategies.

Segmenting crypto users by wallet age and holdings

On-chain data-based user segmentation can take many forms, as there are several characteristics a business can use to compare crypto wallets. However, for the purposes of this exercise, we’ll focus on two simple ones: overall holdings and wallet age. By separating wallets along those two axes, we came up with six separate segments, though of course an exchange could look at more segments if they separated wallets more granularly.

- Early retail: Wallets active since before January 1, 2020 with holdings below $10,000 USD.

- Early professional: Wallets active since before January 1, 2020 with holdings between $10,000 and $10 million.

- Early institutional: Wallets active since before January 1, 2020 with holdings above $10 million.

- Late retail: Wallets that became active on or after January 1, 2020 with holdings below $10,000.

- Late professional: Wallets that became active on or after January 1, 2020 with holdings between $10,000 and $10 million.

- Late institutional: Wallets that became active on or after January 1, 2020 with holdings above $10 million.

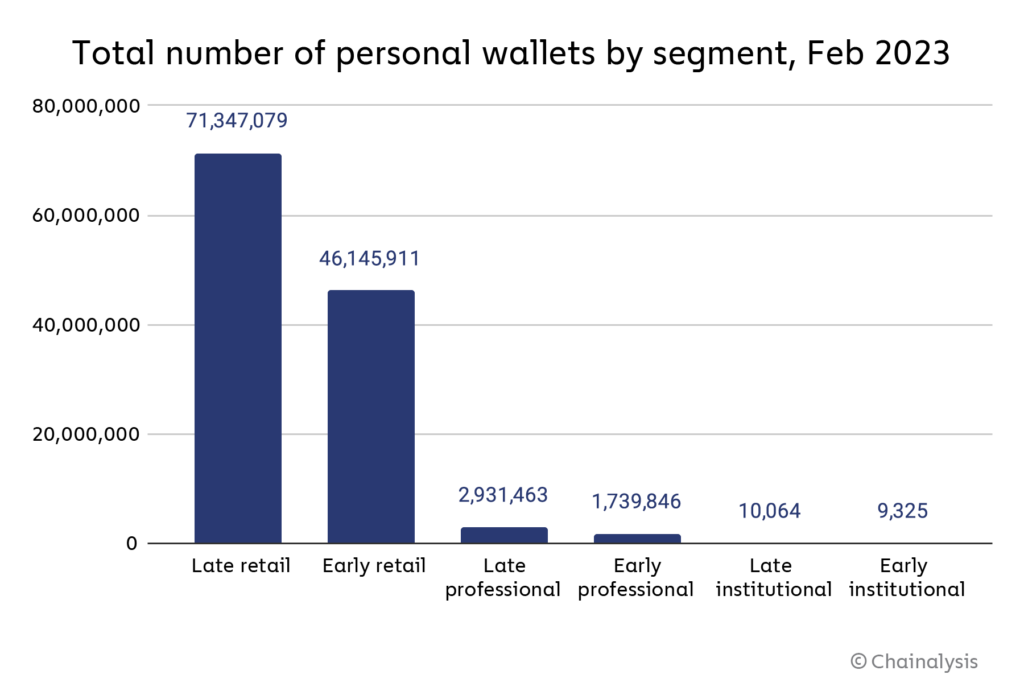

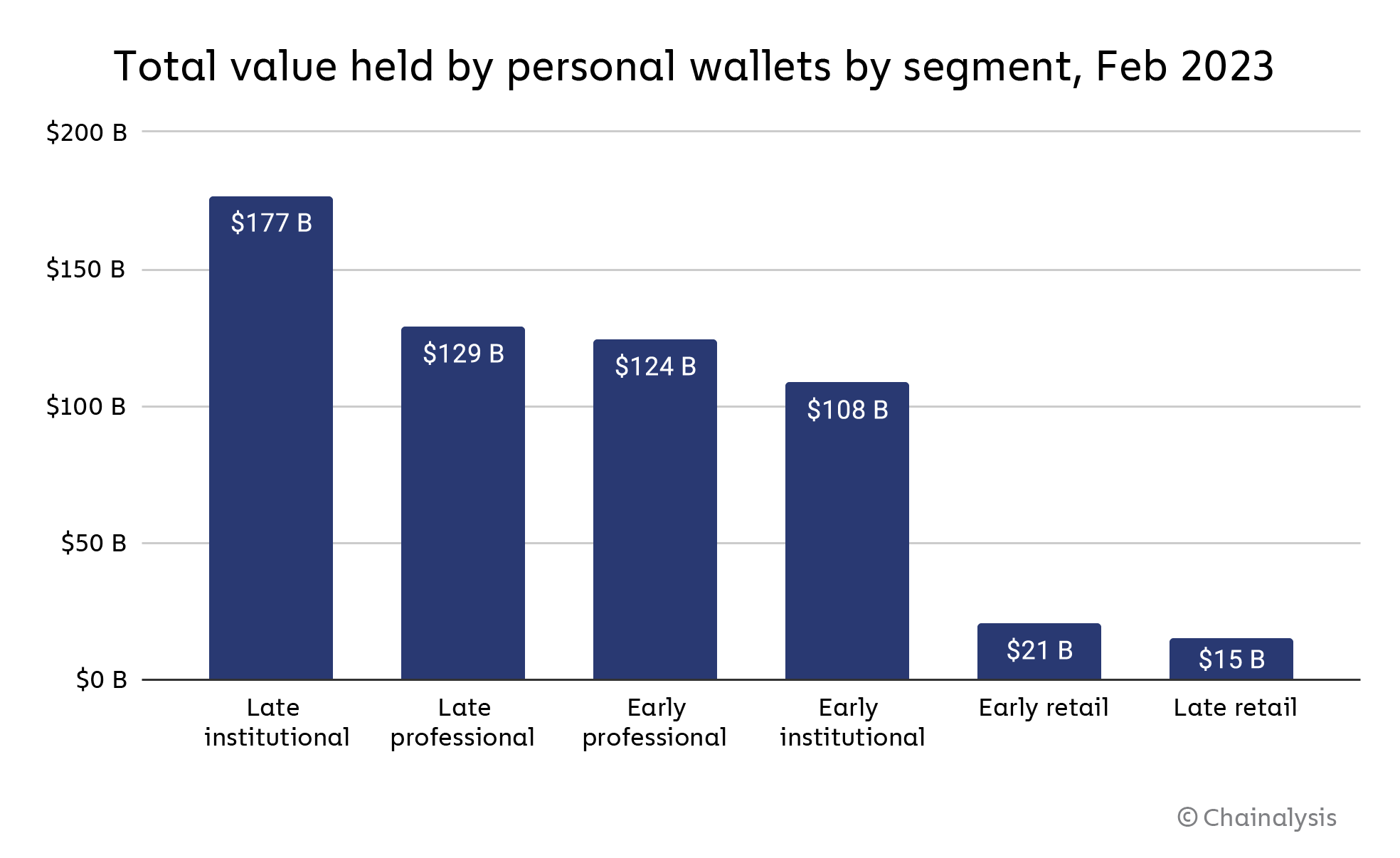

Here’s what those segments look like across the Bitcoin and Ethereum blockchains.

| Segment | Value held by segment | Number of personal wallets | Average held per wallet | Average active weekly wallets |

| Early retail | $20,629,986,812 | 46,145,911 | $447 | 249,768 |

| Early professional | $124,348,073,934 | 1,739,846 | $71,471 | 142,148 |

| Early institutional | $108,472,035,881 | 9,325 | $11,632,390 | 1,595 |

| Late retail | $15,454,498,456 | 71,347,079 | $217 | 10,440,095 |

| Late professional | $129,011,881,592 | 2,931,463 | $44,009 | 1,745,170 |

| Late institutional | $176,802,248,828 | 10,064 | $17,567,791 | 4,309 |

The vast majority of active wallets in a given week are those in late retail, meaning relatively new, low-balance wallets. Interestingly, there are also far more active wallets in the late professional segment than the early retail segment, which underscores just how many people have come to cryptocurrency in recent years and made significant investments, while many earlier entrants have either dropped out, shifted their activity to new wallets, or embraced a passive long-term holding strategy. Overall, late retail wallets represent the majority of all wallets by a wide margin, but command the least capital.

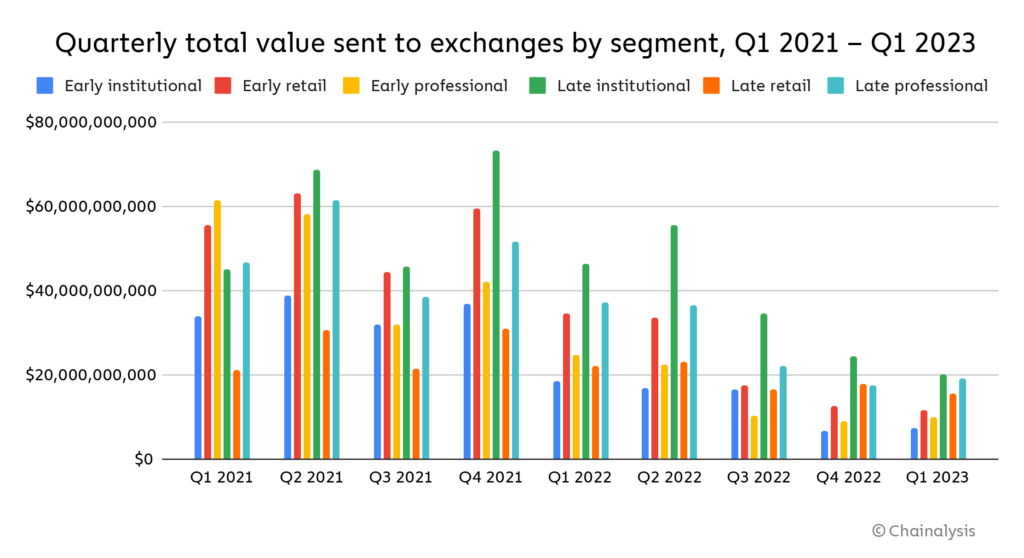

Overall, the relative newcomer groups of late institutional and late whale wallets account for the majority of Bitcoin and Ether currently held by personal wallets. But the more important question for this exercise is, how do these segments interact with exchanges? Centralized exchanges generally make money from trading fees. While we don’t have the insight into exchange order books necessary to calculate fees generated by each segment — all we have is on-chain data — let’s assume that the total funds transferred on-chain to exchanges from each segment roughly tracks with trading fees generated from each segment. Crypto is typically sent from personal wallets to exchanges to be traded rather than held, so this seems like a reasonable assumption.

Since the start of 2021, late institutional wallets account for the biggest share of value sent to centralized exchanges by personal wallets at 23.6%. However, both late professional and early retail wallets are close behind at 18.8% and 19.0% respectively. Overall, in most quarters there’s relative parity among segments in value sent to exchanges, with the exception of late retail wallets and early institutional wallets, which account for 11.4% and 11.9% respectively of total value sent to exchanges during this time period. Both segments exhibit this lag for different reasons — late retail wallets because they command the least capital compared to other segments, and early institutional wallets because they make up the lowest share of all active wallets.

Testing segment analysis on a real exchange: FTX case study

Our wallet-based user segments differ in how they interact with exchanges, but what do those differences mean for exchanges? And how can the people running exchanges translate segment behavior into a successful acquisition and retention strategy? We’ll explore this below using on-chain data from a real, widely used exchange: FTX. While FTX of course collapsed in November 2022, before that it was one of the most popular exchanges in the industry, with a huge, active user base. The on-chain footprint of those users in the months before FTX’s demise give us a large, real-world dataset to analyze through the lens of our user segmentation framework.

Download the full report here to learn how wallets across our six segments interacted with FTX, and see the insights exchanges can get from on-chain user segmentation!