This past week saw three mid-sized banks fail, prompting fears of a bigger, panic-induced bank run. While those fears remain, it appears that depositors at the three banks shuttered over the weekend — Silicon Valley Bank (SVB), Silvergate Bank, and Signature Bank — will be able to access their funds.

All three bank failures have significant implications for cryptocurrency. USDC issuer Circle had $3.3 billion deposited with Silicon Valley Bank, which represented roughly 8% of the dollars backing USDC. Concerns over those deposits prompted USDC to lose its peg over the weekend, and while the peg has since been regained, the incident raises questions about off-chain counterparty risk for stablecoin issuers and other crypto businesses.

The shutdowns of Silvergate and Signature are likely even more significant, as the two were among the largest U.S. providers of banking services to cryptocurrency businesses. While this doesn’t send the cryptocurrency industry back to the stone age of the early 2010s, when it was virtually impossible to get banking partners, these closures significantly limit U.S. banking options in the space and could make it harder for crypto businesses to enable off-ramping into the U.S. dollar. Below, we’ll look at a few data points that explain what happened over the weekend and what could be in store for crypto in the near future.

Crypto fled custodial platforms as USDC depegged amidst Silicon Valley Bank’s failure

SVB provided business banking services to a huge number of venture-backed tech startups. When word began to spread that the bank could be insolvent, as government bonds it purchased in the last few years were now drastically declining in value following recent interest rate hikes, many of those firms moved to pull their money out of SVB. The bank run was the final nail in the coffin, and many SVB customers were unable to transfer their funds before the bank entered into receivership and withdrawals were paused.

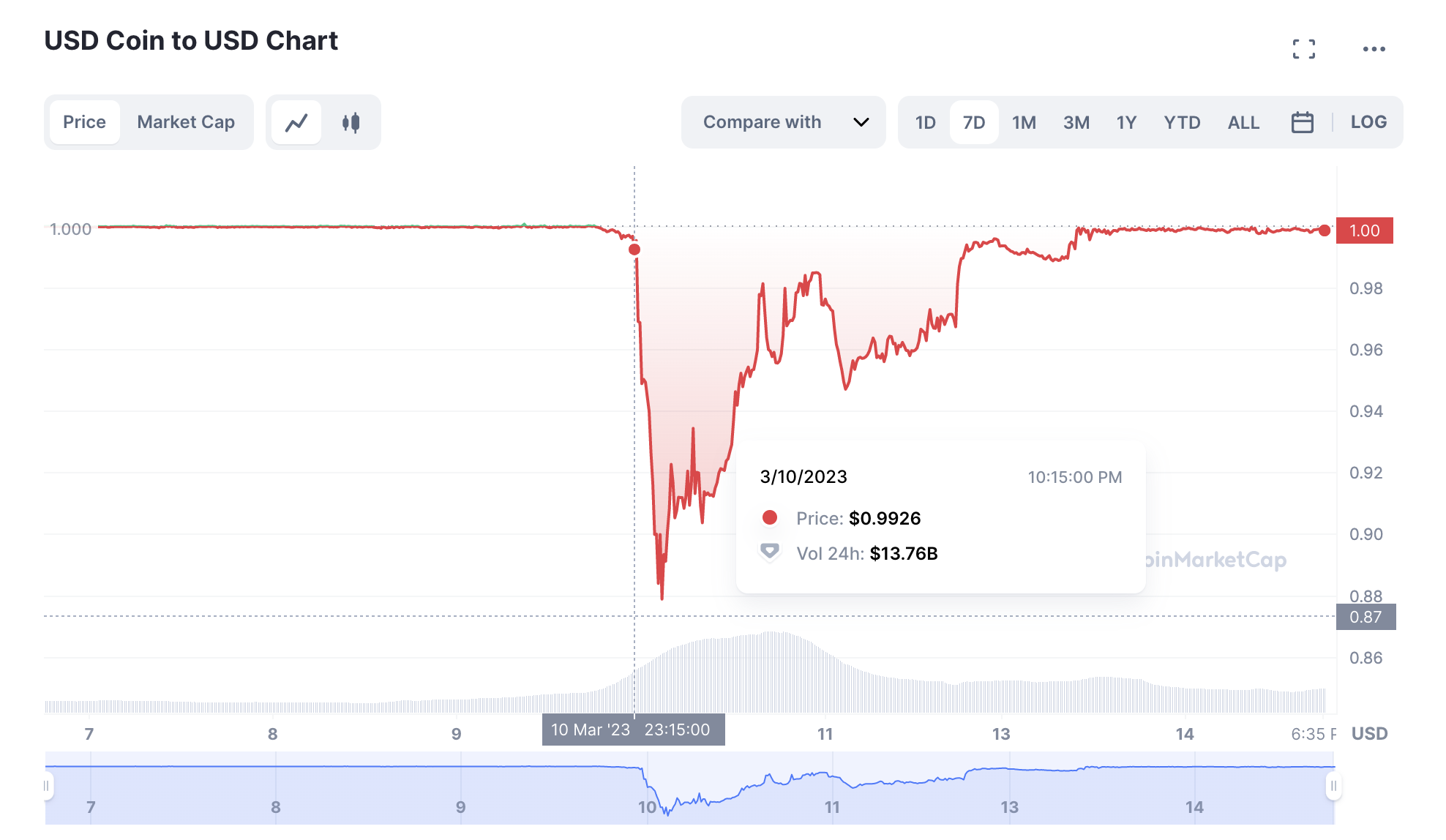

SVB counted many crypto businesses amongst its partners, but none more significant to this story than Circle, the issuer of the highly popular stablecoin USDC. Soon after 10pm ET on Friday, March 10, Circle confirmed circulating speculation and announced that it had $3.3 billion stuck in SVB — roughly 8% of the reserves backing USDC. USDC lost its peg to the U.S. dollar almost immediately after.

Source: CoinMarketCap

By 2am on March 11, just a few hours after Circle’s announcement, USDC’s value had plummeted to $0.87, and while it recovered some, it remained under its $1 target throughout the weekend. This hurt the value of crypto holdings for many, and triggered the liquidation of several trading positions throughout the crypto world.

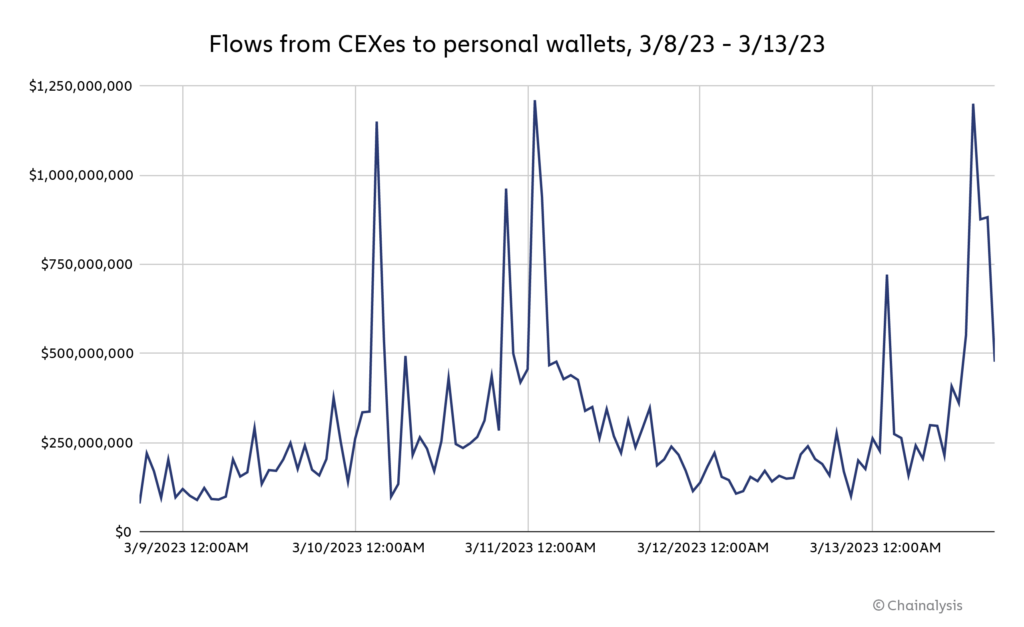

As is often the case in times of market turmoil, outflows from centralized cryptocurrency businesses spiked, likely because users feared they could collapse and leave them unable to access funds, as happened to so many following FTX’s failure.

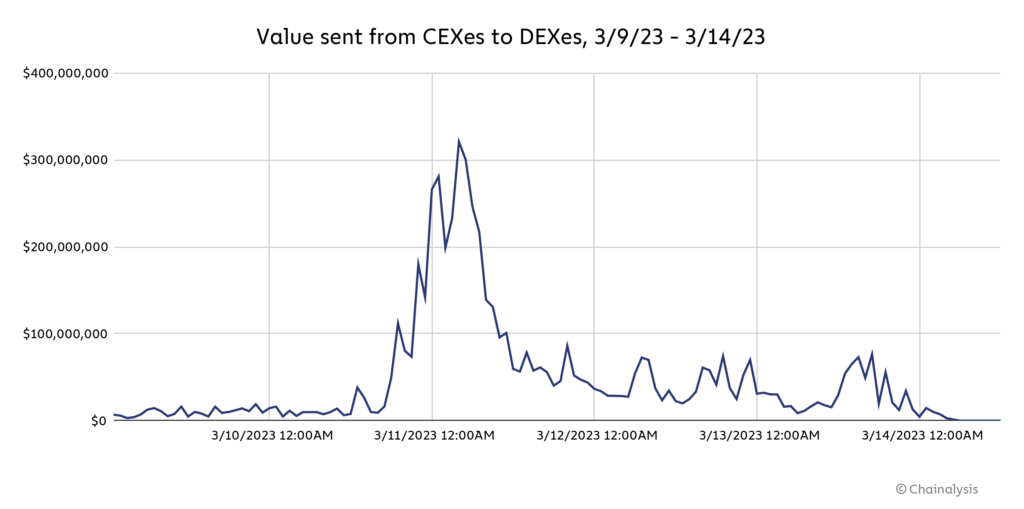

Hourly outflows from centralized exchanges spiked to $1.2 billion at 1am on March 11. A significant portion of those funds were then used for trading at decentralized exchanges (DEXes).

Unsurprisingly given that it depegged and was at the center of the chaos, USDC was one of the top assets being moved to DEXes during this time, as many probably moved to dump their holdings in exchange for other coins while CEXes halted USDC trading.

Wrapped Ether (wETH) also saw a brief spike in transfer volume to DEXes, though we believe this more likely reflected an influx of funds from traders looking to take advantage of the volatility in the market.

What assets did crypto investors turn to during the chaos?

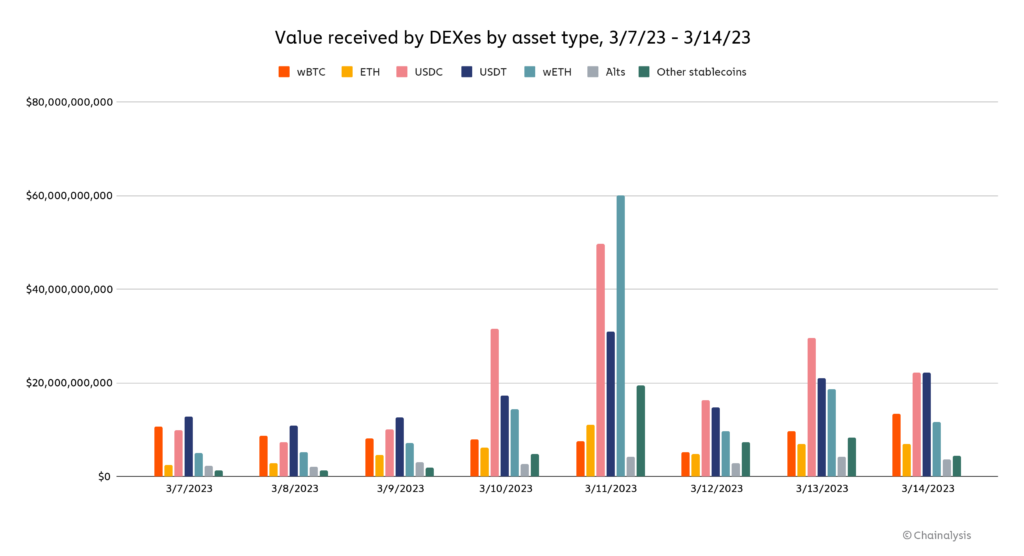

While we know that traders were moving USDC and wETH to DEXes in large volumes during the chaos last weekend, what assets were they acquiring? We’ll look at data from two different DEXes to learn: Curve Finance, which facilitates swaps of stablecoins only, and Uniswap, which facilitates swaps of virtually all Ethereum-based crypto assets. Together, the two DEXes represent a huge share of total DEX transaction volume, so they should provide a representative sample of what assets investors turned to during this time.

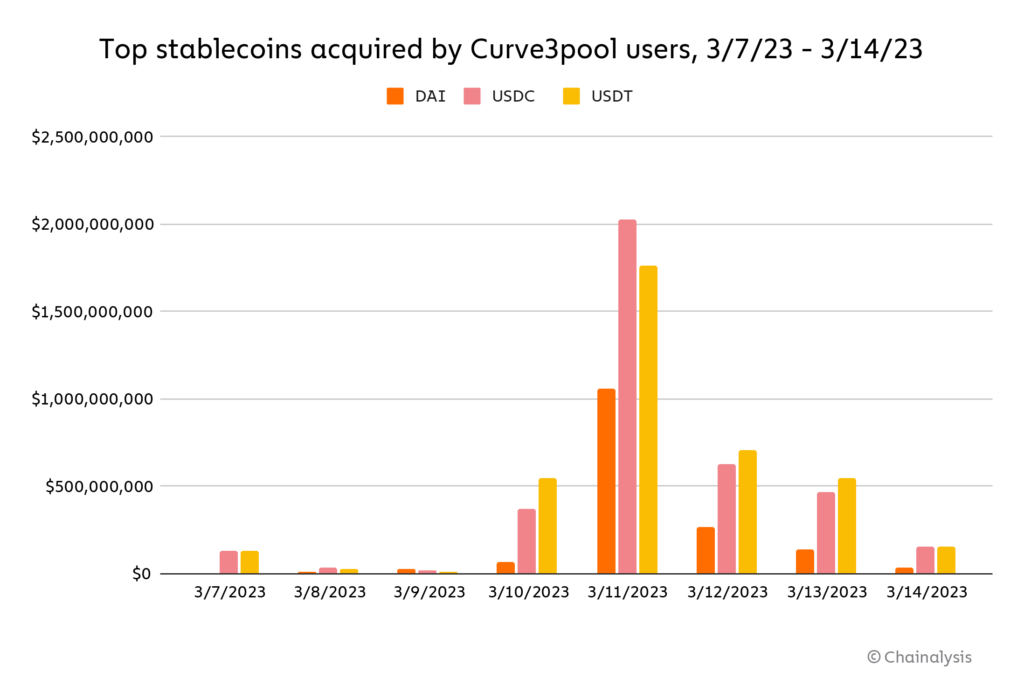

First, let’s look at Curve.

Curve saw acquisitions of USDT and DAI spike over the weekend as USDC depegged — but oddly enough, USDC saw an even bigger spike. This may suggest that some traders foresaw USDC regaining its peg, and sought to acquire it in bulk at a discount.

What do we see on Uniswap during this time?

Once again, several assets saw large spikes in user acquisition, but none more than USDC. Outside of stablecoins, wETH also saw a spike in acquisition volume. Similar to USDC, wETH (and, of course, Ether itself) also saw a drop in volume this weekend, which was quickly recovered by end of day Sunday when it became clear the banking crisis was, for the time being, over. In fact, by Tuesday March 14, ETH/wETH hit $1,773, breaking its three-month high, and currently sits at $1,660, which is good news for traders who moved to acquire it over the weekend.

Ether isn’t the only crypto asset that’s seen positive price movement since the resolution of the SVB issue. Bitcoin followed a similar pattern, falling from $22,150 on March 8 to a one-month low of $19,670 on Friday the 10th, but then recovered to a three-month high of $26,000 on Tuesday. That price action suggests elevated demand for Bitcoin in recent days. We don’t see that reflected on DEXes, as wrapped Bitcoin (wBTC — Bitcoin’s ERC-20 equivalent) didn’t see a large increase in acquisition volume during the time period studied. That means any elevated purchasing of Bitcoin likely happened on CEXes, meaning the data for it isn’t on-chain.

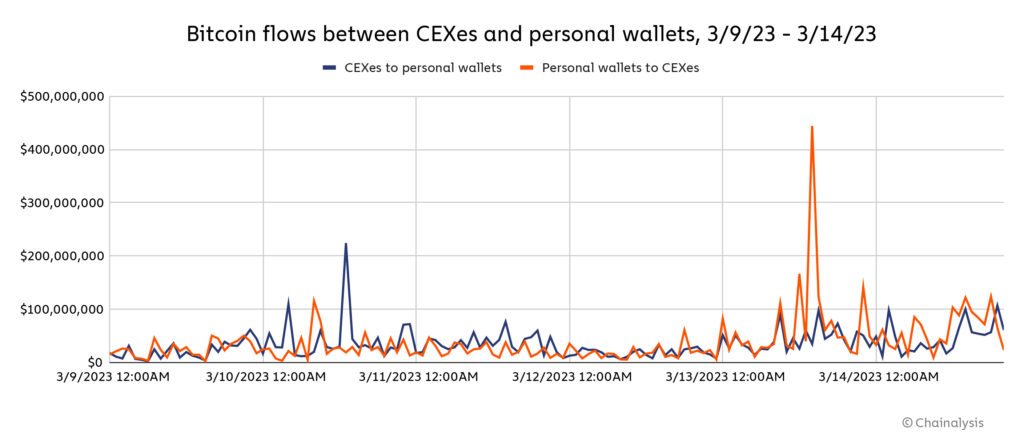

We can, however, use on-chain data to see how Bitcoin moved between exchanges and personal wallets during this time period.

We see a huge spike in Bitcoin sent from CEXes to personal wallets on Friday, March 10, at a time when the SVB situation was looking dire but USDC had yet to depeg. Could that have reflected users’ concerns about their exchange deposits being available in the event of a major crisis? We can’t know for sure, but it’s possible that some large Bitcoin holders moved their Bitcoin to personal wallets to ensure it would be accessible in a worst-case scenario. On Monday the 13th, when the SVB issue was resolved, we saw an even bigger movement in the opposite direction, with a huge spike in Bitcoin sent from personal wallets back to CEXes. This came following a large jump in Bitcoin’s price, and may reflect traders’ desire to take advantage and sell, or at least have their Bitcoin ready on an exchange to sell in the event of further price jumps.

What’s next? Watch for liquidity issues in absence of crypto banks

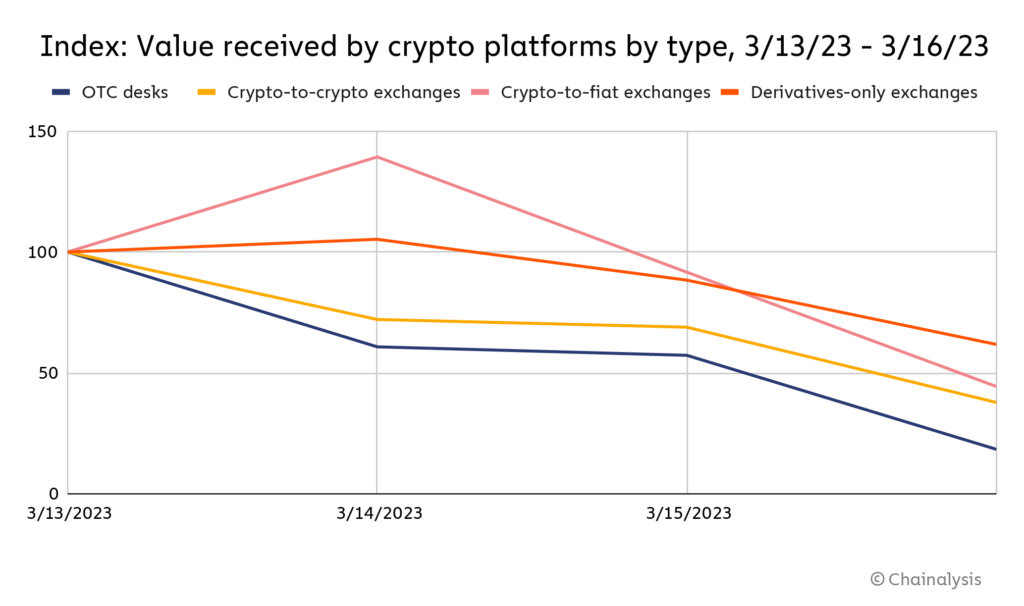

While depositors at the banks that failed over the weekend can rest easy, the threat of further bank crises remains, and there’s still one major crypto-specific issue: two of the primary banks the industry relied on are gone. With two crucial on and off-ramps between crypto and the U.S. dollar now gone, we could see lower liquidity and therefore lower transaction activity in crypto markets. So far, transaction activity across all major platform types has dipped since Monday, March 13, though it remains within normal ranges.

OTCs in particular are worth watching, as they typically execute some of the biggest transactions, especially large cash-for-crypto trades. Over the next several weeks, we’ll be watching their activity along with that of other platforms to get a sense of how bank closures have impacted market dynamics.

Not Investment or Other Advice

This material is for informational purposes only, and is not intended to provide legal, tax, financial, or investment advice. Recipients should consult their own advisors before making these types of decisions. Chainalysis does not guarantee or warrant the accuracy, completeness, timeliness, suitability or validity of the information herein. Chainalysis has no responsibility or liability for any decision made or any other acts or omissions in connection with Recipient’s use of this material.